YouTube has terminated “Looksmaxxing” influencer and streamer Clavicular‘s two channels for “severe or repeated violations.”

The controversial creator, whose real name is Braden Peters, took to X on Thursday to ask his fans to help recover his @LiveWithClav and @ClavLooksmax accounts.

“Very sad news this morning. My YouTube channels @ LiveWithClav & @ ClavLooksmax were terminated this morning with no warning or explanation,” he wrote. “The channels consisted of livestream VODs and free courses created by me to help empower young men to be the best versions of themselves.”

The streamer continued, “Me and my team worked hard to ensure we followed YouTube’s TOS very strictly, blurring out all inappropriate language and sensitive topics. Could you please help in recovering my accounts?”

Though Clavicular claims YouTube didn’t give him an explanation for the move, in the emails he received from the video platform, it clearly listed community guideline violations as the reason.

The platform also gave Clavicular the same explanation for removing both accounts. “We have reviewed your content and found severe or repeated violations of our Community Guidelines. Because of this, we have removed your channel from YouTube,” the emails read.

When The Hollywood Reporter reached out to YouTube for more information, a spokesperson explained that Clavicular’s original channel was terminated last year for “facilitating access to websites that violate our Illegal or regulated goods or services policies,” and that these were just additional accounts.

“We terminated the creator’s original channel back in November 2025. We removed these additional channels under our terms of service, which prohibit creating new channels after a termination,” the YouTube spokesperson wrote in a statement to THR.

The platform prohibits creators from owning or creating new channels following a termination.

This came just over a week after Clavicular was hospitalized for a suspected overdose. He was livestreaming at a mall and restaurant in Miami on Kick when the incident happened.

He went home the following day and shared an update on X at the time: “Just got home, that was brutal. All of the substances are just a cope trying to feel neurotypical while being in public, but obviously that isn’t a real solution. The worst part of tonight was my face descending from the life support mask.”

The U.S. Department of Justice arrested a Master Sergeant with the Army on allegations he placed wagers on the raid of Nicolas Maduro ahead of participating in the operation to detain former Venezuelan leader.

The DOJ unsealed an indictment Thursday charging Gannon Ken Van Dyke with the unlawful use of confidential government information for personal gain, theft of nonpublic government information and fraud charges, alleging he used his knowledge of the forthcoming raid on Venezuela to place $33,000 in bets, winning about $400,000 after the raid.

“The defendant allegedly violated the trust placed in him by the United States Government by using classified information about a sensitive military operation to place bets on the timing and outcome of that very operation, all to turn a profit,” U.S. Attorney Jay Clayton said in a statement. “That is clear insider trading and is illegal under federal law.”

Van Dyke allegedly created a Polymarket account on Dec. 26, 2025 and placed 13 bets through Jan. 2, 2026 on contracts expecting whether U.S. forces would land in Venezuela, remove Maduro, invade Venezuela and similar contracts.

Van Dyke is also an active duty soldier with the Army’s special forces, based out of Fort Bragg. According to the indictment, he “was involved in the planning and execution” of the military operation to detain Maduro.

After the raid, Van Dyke allegedly withdrew the funds, converted the winnings to a bridged version of USDC, sent them to “a foreign cryptocurrency ‘vault’” and then began withdrawing funds and moving them into a brokerage account, the filing said.

The filing noted that the fact someone had made a massive profit on these Polymarket bets had been noticed by news organizations, and alleged that Van Dyke asked Polymarket to delete his account and changed his email to conceal his identity.

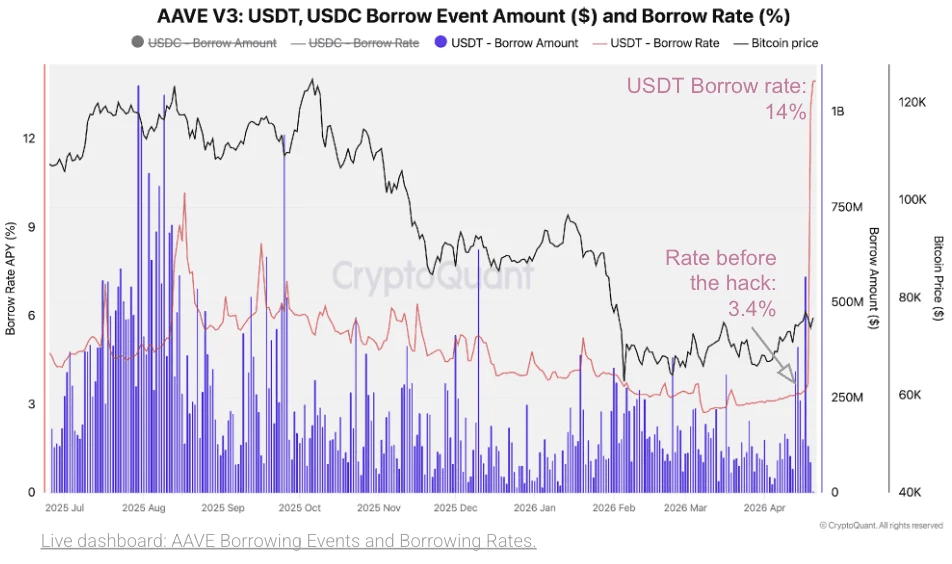

The KelpDAO exploit allowed an attacker to siphon unbacked rsETH tokens and deposit them into Aave, triggering one of the sharpest liquidity contractions in recent DeFi history, according to the latest Cryptoquant report dubbed the “ DeFi Contagion.”

Key Takeaways:

The KelpDAO exploit on April 18, 2026, exposed Aave to an estimated $124M-$230M in bad debt within 72 hours.

Aave’s total value locked fell 33%, shedding billions, with $USDT and $USDC borrow rates hitting 14%.

$USDe supply shed $800 million in three days, signaling continued DeFi liquidity stress across major protocols.

KelpDAO rsETH Hack Triggers Multi-Billion-Dollar Liquidity Drain on Aave

According to Cryptoquant’s assessment of the situation, the attacker used the drained uncollateralized rsETH to exchange for WETH and stablecoins on Aave, exploiting a critical vulnerability in KelpDAO’s infrastructure. The attack quickly rippled across the broader DeFi ecosystem.

Cryptoquant researchers found that Aave’s aETHrsETH contract holds approximately 83% of all rsETH circulating supply, making it the single most exposed protocol to the hack. The firm estimates Aave now carries between $124 million and $230 million in potential bad debt tied to depegged rsETH collateral.

Aave’s total value locked (TVL) dropped massively in the 72 hours following the exploit, a 33% drop that Cryptoquant described as one of the sharpest protocol-level liquidity contractions in recent DeFi history.

Borrowing rates across Aave’s three largest markets reflected the pressure immediately. Cryptoquant data shows $USDT and $USDC borrow rates on Aave V3 jumped from 3.4% to 14% as users rushed to borrow stablecoins and exit the protocol. Before the hack, those rates had held steady at 3.4%, consistent with normal DeFi lending conditions.

$ETH borrowing rates on Aave V3 climbed to 8%, the highest reading Cryptoquant has recorded since at least January 2024. Rates later stabilized near 5%, still more than double the pre-hack level of 2%.

The simultaneous rate spike across $ETH, $USDC, and $USDT signals system-wide stress rather than isolated market movement, according to the Cryptoquant report. $ETH, $USDC, and $USDT are Aave’s three largest markets by total value locked.

Cryptoquant researchers described the dynamics as a classic DeFi liquidity crunch: depositors withdrawing while borrowers increase demand at the same time, leaving available liquidity to fall rapidly and interest rates to reset higher. As of the report date, rates remain elevated above pre-hack levels.

The yield-bearing stablecoin, $USDe, the fourth-largest asset on Aave with $412 million in protocol deposits, also saw significant pressure. Cryptoquant tracked a net collapse in $USDe minting activity in the days following the hack, driven by both contagion from the Aave crisis and persistently negative $ETH and BTC perpetual futures funding rates.

$USDe’s total supply fell from $5.8 billion to $5 billion in three days, a decline of $800 million or 14%. Cryptoquant called it one of the largest short-term redemption events in $USDe’s history.

As one of the largest stablecoins globally behind only $USDT, $USDC, USDS, and DAI, $USDe’s contraction points to a meaningful withdrawal of liquidity from the broader DeFi ecosystem, the firm noted.

Negative perpetual funding rates compressed $USDe’s delta-neutral yield during this period, accelerating redemption incentives for holders. Cryptoquant explained that the combination of hack-driven risk-off behavior and structural funding rate pressure marks a significant deterioration in DeFi market conditions.

The latest Cryptoquant report highlights the systemic risk of concentrated collateral exposure in DeFi lending protocols, noting that Aave‘s outsized rsETH position amplified contagion far beyond the initial exploit.

Pretty much every other year since 2002, Graydon Carter — first as editor of Vanity Fair, then as founder and editor of Air Mail — has hosted a party during the Cannes Film Festival that has reliably been the most coveted invitation in a week packed with star-studded affairs. Hosted at the Hotel du Cap-Eden-Roc in Antibes, the bacchanal was long a Mediterranean corrolary to VF’s Oscar Party, where A-listers were less likely to talk business and more likely to jump in the pool fully clothed.

The bash last made headlines when Carter’s then co-host — basic cable exec turned Warner Bros. CEO David Zaslav, whose self-enriching stewardship of the studio earned him few friends in Hollywood — drew mockery for aping Carter’s style. This year, on May 19, Carter will co-host his first Cannes party since leaving Air Mail last October. His co-hosts this time will be the ultimate Hollywood insider, CAA co-chairman and CEO Bryan Lourd, and an industry outsider: the ascendant Silicon Valley tycoon Dario Amodei, CEO of the AI company Anthropic.

Carter and Amodei may seem an odd pairing: the worldly, print-worshipping, bon-vivant old-media titan and the socially awkward, studiedly unflashy scientist presenting himself as the safe, responsible contender the race to shape the future of AI. Unlike his more extroverted rival and former boss Sam Altman of OpenAI, whose ill-fated forays into Hollywood have been well documented, Amodei seems to have no interest in breaking into the entertainment business. But the bedfellows are less strange when you remember that Carter launched the Vanity Fair New Establishment, and annual ranking of the most powerful people in tech and business, which later turned into an annual San Francisco summit of the same name, gathering the biggest names in Silicon Valley. And with Altman’s reputation having suffered a fewdings lately, there is arguably no bigger name than Amodei at the moment.

“AI has more or less become a driving force in today’s culture,” Carter told The Hollywood Reporter in an email interview. “Dario came to dinner last year and honestly, after talking to him, I felt like I had been working in wood. He’s been among the most thoughtful and candid voices engaging with the questions AI raises and seems to genuinely want to hear from people outside of tech.”

Following that evening in New York, Carter reached out to Amodei with an offer to co-host and help pay for the party at the Hotel du Cap. Both stand to benefit: Carter proves he still has the swagger and clout after his contentious departure from Air Mail (following its acquisition by Puck, the media outlet founded by his former assistant and protégé Jon Kelly) to keep throwing his signature Cannes party and to team up with one of the most powerful young CEOs in the world. Amodei, meanwhile, will be given the chance to break out of the Silicon Valley bubble and be introduced to cultural movers and shakers.

There’s little risk of Amodei pulling a Zaslav and ripping off Carter’s wardrobe. Though he presumably owns a tux at this point, he was influenced early on by effective altruism, a philanthropic movement known for scorning frivolity (e.g. black-tie galas, or, well, Hollywood parties) in favor of more data-driven ways of helping the afflicted (e.g. by creating safe AI).

“He reminded me more of a philosopher than a tech leader,” says Carter of his dinner with Amodei. “I found him to be deeply thoughtful, curious about the world, and — a rarity for Silicon Valley — honest.”

Aside from the presence of Amodei, the party will likely feel familiar to those who have attended in the past. “I’ve given this dinner at the Hotel du Cap off and on for the past 25 years. And it’s one of the few big events that I’ve actually enjoyed,” says Carter. “Many of the old Vanity Fair hands are involved — so it doubles as a sort of reunion. And the guest list is stellar.” Carter won’t share names, but given his track record, he wouldn’t bandy the word “stellar” about lightly.

One confirmed attendee is Lourd. “I’ve known Bryan for decades and he’s the closest thing Hollywood has to a mayor,” says Carter. “Who wouldn’t want to partner with him?” (Carter, a producer on several films, says he remains involved in the business, with a number of documentary and TV projects in the works.)

Carter has made no secret of his fondness for all things analog, from film to paper, another reason his partnership with Amodei might raise eyebrows. But he admits to using Anthropic’s flagship chatbot, Claude, on occasion. “I’ve found Claude to have a sort of pen-and-paper quality to it. It functions like one of the best assistants I had back in the Vanity Fair days — except that it doesn’t need water and doesn’t dream of becoming an editor one day.”

Asked what the last thing he’s used it for is, Carter says, “Drumming up appropriate answers to really difficult questions like these.”

YouTube has pulled down two channels operated by Braden Peters, the “looskmaxxing” streamer who is known online as Clavicular.

In November 2025, YouTube had terminated Clavicular’s original channel for facilitating access to websites that violate the platform’s Illegal or regulated goods or services policies, according to a YouTube spokesperson. YouTube’s terms of service prohibit creators from creating or owning new channels after a termination.

“We terminated the creator’s original channel back in November 2025,” a YouTube rep told Variety. “We removed these additional channels under our terms of service, which prohibit creating new channels after a termination.”

Clavicular posted Thursday on X about the YouTube channel removals. “Very sad news this morning. My YouTube channels @ LiveWithClav & @ ClavLooksmax were terminated this morning with no warning or explanation,” he wrote. “The channels consisted of livestream VODs and free courses created by me to help empower young men to be the best versions of themselves. Me and my team worked hard to ensure we followed YouTube’s TOS very strictly, blurring out all inapproriate [sic] language and sensitive topics. Could you please help in recovering my accounts?” His post tagged @TeamYouTube, @YouTubeCreators and @YouTube.

Images that Clavicular posted of notices he received from YouTube about the channel removals said, “We have reviewed your content and found severe or repeated violations of our Community Guidelines. Because of this, we have removed your channel from YouTube.”

Clavicular is a prominent face of the “looksmaxxing” movement, which has been defined an “online self-improvement practice focused on the process of maximizing one’s own physical attractiveness.”

Last week, the 20-year-old Peters was reportedly hospitalized in Miami after he is believed to have suffered an overdose during a livestream. “Just got home, that was brutal,” he wrote in an April 15 post on X. “All of the substances are just a cope trying to feel neurotypical while being in public, but obviously that isn’t a real solution. The worst part of tonight was my face descending from the life support mask.”

Deloitte and Touche LLP has completed a SOC 2 Type 2 examination for Chainlink’s CCIP and Data Feeds, making Chainlink the only data and interoperability oracle platform in the blockchain industry to hold SOC 2 Type 2, SOC 2 Type 1, and ISO/IEC 27001:2022 certifications simultaneously, the full stack of security credentials that institutional risk teams require before deployment.

Chainlink announced on X that Deloitte and Touche LLP has completed a SOC 2 Type 2 examination for Chainlink CCIP and Data Feeds, including Price Feeds and SmartData feeds such as Proof of Reserve and Net Asset Value. The examination was performed in accordance with attestation standards established by the American Institute of Certified Public Accountants, the same regulatory standard used across the traditional financial services industry.

Chainlink SOC 2 Type 2 Deloitte Certification Completes the Full Institutional Security Stack

SOC 2 Type 2 is distinct from Type 1 in a critical way: where Type 1 evaluates whether security controls are designed correctly, Type 2 evaluates whether those controls actually operate effectively over a sustained period of time. For institutional risk teams, legal departments, and compliance officers at banks and asset managers, that operational verification is the one they require before approving deployment of any technology vendor. Chainlink previously achieved SOC 2 Type 1 attestation and ISO/IEC 27001:2022 certification, establishing a compliance benchmark no other oracle platform had reached. The Type 2 result now closes the final gap between Chainlink’s compliance posture and the requirements of the most conservative institutional buyers in traditional finance. As crypto.news reported, CCIP has been averaging approximately $90 million in weekly token transfers and Chainlink’s oracle infrastructure has enabled over $28 trillion in cumulative transaction value, providing a production track record that the Type 2 certification now formally validates through an independent third party.

What the Certification Unlocks for Institutional Deployment

SOC 2 Type 2 attestation from a Big-4 accounting firm is not a technical upgrade, it is a procurement unlock. Large financial institutions including banks, asset managers, pension funds, and insurance companies operate under vendor due diligence frameworks that require external attestation of security controls before any third-party technology can be approved for production use. An internal security claim from a blockchain protocol carries no weight in that process. A Deloitte attestation does. As crypto.news documented, the tokenized real-world asset sector hit $27 billion in 2026, with Chainlink positioned as the primary oracle infrastructure for the growing pipeline of institutions tokenizing equities, funds, and bonds on-chain. The SOC 2 Type 2 result strengthens that position by removing the final compliance objection that regulated institutions commonly raise against blockchain technology vendors. Institutions already using Chainlink, including Swift, Euroclear, JPMorgan, UBS, and Fidelity International, operate under exactly the compliance frameworks the Type 2 attestation addresses.

$LINK Price Has Not Reflected the Fundamental Progress

Despite the certification and the broader institutional adoption narrative, $LINK has remained under price pressure in 2026. As crypto.news tracked, Chainlink signed an exclusive CCIP partnership with SBI Digital Markets in late 2025, positioning itself as the cross-chain infrastructure for SBI’s full digital asset hub across issuance, settlement, and secondary trading. The SBI deal, the Deloitte certification, and the live equity data stream rollout all point in the same structural direction: Chainlink is becoming embedded in regulated financial infrastructure at a pace that most market participants are not currently pricing into $LINK. The token was trading at approximately $9.17 on April 23, roughly 50% below its late 2025 highs, in a market environment where broader macro pressure from the Iran conflict has suppressed risk appetite across digital assets.

Chainlink’s next major institutional milestone is the expansion of its Data Streams product to cover equity market hours globally, with the tokenized RWA sector expected to reach well beyond $27 billion in total value as more financial institutions move from pilot to production deployment.

In December 2024, $PEPE was worth $11 billion. Not the company. Not a project with thousands of employees, a product, or a revenue model. A frog meme coin with an anonymous team, no roadmap, and an official website that openly says it has “no intrinsic value.” Eleven billion dollars.

By April 2026, that same market cap has fallen to approximately $1.6 billion. That’s still an extraordinary valuation for something the creators themselves describe as entertainment.

On April 8, 2026, Canary Capital filed an S-1 with the SEC for the first spot $PEPE ETF — a regulated product that would hold actual $PEPE tokens. The day after the filing, $PEPE dropped 4.58%. Welcome to meme coin investing.

Disclaimer: This is informational analysis only, not investment advice. $PEPE is one of the most volatile assets in crypto. Never invest more than you can afford to lose entirely.

The Origin Story: A $250 Investment, a $1.8 Million Return, and Internet History

$PEPE launched on April 17, 2023. There was no presale. No influencer promotion. No venture capital. No tax on transactions. No utility. No roadmap. Just an ERC-20 token on Ethereum, named after Pepe the Frog — the internet’s most versatile meme character, created by artist Matt Furie in a 2005 comic called “Boy’s Club.”

The first notable trade became the stuff of crypto legend: someone swapped 0.125 ETH (worth approximately $250 at the time) for 5.9 trillion $PEPE tokens. By April 19 — two days after launch — those tokens were worth approximately $1.8 million. That’s a 7,200x return in 48 hours.

That single trade went viral. Twitter flooded with screenshots. Telegram groups exploded. Retail traders who had been sitting on the sidelines watching Bitcoin’s steady climb suddenly saw a path to the kind of returns they’d missed in 2021. $PEPE wasn’t trying to be the next Ethereum. It was trying to be the next Dogecoin. And for a moment, it almost was.

Within weeks of launch, $PEPE’s market cap hit $1.6 billion. Within 18 months, it would hit $11 billion.

The official $PEPE website states this plainly: “$PEPE has no affiliation with Matt Furie or the Pepe the Frog IP. $PEPE is a meme coin without intrinsic value or expectations of financial returns. It lacks a formal team or a developmental roadmap, existing solely for entertainment.”

That honesty is almost refreshing in a space where every project claims to be “revolutionising” something.

The tokenomics match the philosophy: 420,690,000,000,000 total supply (420.69 trillion, the number a direct nod to cannabis culture’s 4/20). Of that, 93.1% was sent to the Uniswap liquidity pool and the LP tokens were burned — permanently. The deployer contract was sent to a null address, meaning the team renounced ownership. The remaining 6.9% was placed in a multi-sig wallet for future centralized exchange listings, bridges, and additional liquidity pools.

No inflation. No ongoing issuance. Fixed supply. Nearly all of it in circulating markets. From a tokenomics standpoint, $PEPE is cleaner than many “serious” projects.

The Two All-Time Highs and What Drove Each

$PEPE’s price history has two distinct chapters, and they’re driven by completely different forces.

Chapter One: The 2023 Meme Coin Spring

The first $ATH of approximately $0.000004213 arrived on May 5, 2023 — just 18 days after launch. This was almost entirely driven by retail momentum, Twitter virality, and the $250-to-$1.8M story spreading across crypto social media. The $1.6 billion market cap at that point was remarkable for a token that had been live for under three weeks.

Then reality arrived. The initial frenzy always cools. By September 2023, $PEPE had declined to $0.0000006 — an 85% drop from the first $ATH. That’s a pattern anyone who has followed meme coins recognises: explosive launch, spectacular fade, long sideways grind.

But in August 2023, something more specific happened that compounded the decline. Rogue members of the original development team moved 16 trillion $PEPE tokens from the multi-signature wallet to centralised exchanges without authorisation. The team’s official communication channels condemned the action — describing it as theft by “disgruntled former team members” — but the 16 trillion tokens hit the market at the same time the token was already weakening. $PEPE lost roughly 27% in the two days following the disclosure. The multi-sig would later be restructured with different signatories.

Chapter Two: The 2024 Bull Market Peak

The second and dramatically larger $ATH came on December 9, 2024: approximately $0.000028 — giving $PEPE a market cap of over $11 billion.

This move had multiple catalysts that compounded each other. The broader Bitcoin bull market had pushed $BTC through $100,000 in November 2024, triggering an altcoin rotation. Trump’s election victory in November brought a crypto-friendly regulatory environment narrative that sent speculative assets sharply higher. And Robinhood listed $PEPE on November 13, 2024 — the same day Coinbase signalled plans to do so.

Those three things arrived simultaneously: macro bull, political catalyst, and the biggest retail distribution platform in the US opening access to $PEPE. The token went from approximately $0.000011 to $0.000028 in three weeks.

At $0.000028 and $11 billion market cap, $PEPE was worth more than many publicly traded mid-cap companies. The token with no utility, no team, and no roadmap had become a top-20 cryptocurrency.

$PEPE’s December 2024 surge was one of the defining events of the meme coin bull run that BCR tracked in real-time — including the famous case of a $27 early investment turning into $5 million in gains.

Where $PEPE Is Now: April 2026

The current situation is straightforward: $PEPE has given back approximately 86% of its December 2024 peak value.

At approximately $0.0000039 in April 2026, $PEPE’s market cap is roughly $1.6 billion. That sounds like collapse — and from the $ATH it is. But it’s worth noting that $PEPE at $1.6 billion is still:

Larger than when it first launched (May 2023 $ATH was also ~$1.6B, but at 7x the current price — the supply understanding matters here)

Ranked #44 on CoinMarketCap, making it a legitimate top-50 cryptocurrency

Trading $400–800 million in daily volume — more liquidity than most “serious” infrastructure projects

One of only a handful of meme coins that has survived two full bear cycles and maintained genuine exchange presence

BCR’s November 2025 $PEPE analysis correctly identified the $0.0000052 support level as critical, noting that RSI was approaching oversold territory and that open interest had been reset to multi-month lows — suggesting weak hands had largely exited. $PEPE has since bounced modestly from those lows and briefly led a 65% weekly surge in January 2026 when the broader meme coin sector gained 23% in a single week, pushing total meme market cap to $47.7 billion.

The broader BCR prediction page for $PEPE has consistently tracked the tension between $PEPE’s market cap size (which limits explosive upside) and its community depth (which provides a floor during bear markets that most meme coins lack).

The Canary Capital ETF: What It Means and What It Doesn’t

April 8, 2026 was a genuinely historic day for meme coins in general: Canary Capital Group, a Nashville-based asset manager, filed an S-1 registration statement with the SEC for the Canary $PEPE ETF — the first-ever application to launch a regulated, spot-price ETF backed by actual $PEPE tokens.

This is not a derivatives product or a synthetic instrument. If approved, it would hold real $PEPE tokens as its primary asset and trade on a US exchange, giving investors regulated meme coin exposure without needing a crypto wallet, a Coinbase account, or any blockchain knowledge.

The ETF filing matters symbolically for two reasons. First, Dogecoin ETFs had already been approved, establishing precedent that meme coins can qualify as legitimate ETF assets. Second, Canary Capital choosing $PEPE specifically — rather than Shiba Inu or any of the newer Solana-based meme coins — reflects $PEPE’s position as the second-largest meme coin by market cap and the one with the deepest liquidity on established chains.

What followed the filing was revealing about where the market’s head is at. $PEPE dropped 4.58% the day after the filing. Then it recovered and rallied 10% on April 17 on $39.78 million in fresh derivatives inflows — not because anything about the ETF changed, but because derivatives traders saw oversold conditions and piled in.

As BCR’s reporting on the $PEPE vs meme coin landscape noted in late 2025, $PEPE “remains the leading indicator of risk appetite across the meme coin space” — its price movements tend to precede or amplify broader meme coin sector moves.

The honest assessment of the ETF: it adds institutional visibility to $PEPE, and in the medium term (12–24 months), an ETF approval would be the most significant demand catalyst the token has ever seen. But Dogecoin ETFs attracted only $7.64 million in total assets after approval — suggesting that regulated institutional interest in meme coins is real but smaller than headlines suggest. The SEC review could take up to 240 days. Approval is uncertain. And even if approved, the ETF’s impact on $PEPE’s price depends on how much capital actually flows into the product.

$PEPE Key Data (April 2026)

Sources: CoinMarketCap — $PEPE; CoinGecko — $PEPE

The Honest Case For and Against $PEPE

There are two positions on $PEPE, and both are held by people who’ve done serious research. Here’s the genuine version of each.

The bull case:$PEPE at $1.6 billion market cap, 86% below its $ATH, with $400–800M in daily volume, a top-50 rank, and a spot ETF under SEC review is a genuinely interesting asymmetric bet. Reaching the December 2024 $ATH of $0.000028 requires approximately a 7x from current prices. In a broad crypto bull cycle where Bitcoin pushes toward new highs and meme coin narratives reactivate, $PEPE — with its name recognition, liquidity depth, and cultural resonance — is among the last meme coins to get cut from mainstream consciousness. The ETF adds a new demand vector that didn’t exist in the prior cycle. Whale accumulation of 1.23 trillion tokens in a single April session suggests informed capital building positions at current levels.

The bear case:$PEPE has no utility, no product, no revenue, and no development team with defined accountability. The December 2024 peak was driven by a specific combination of catalysts ($BTC $100K, Trump election, Robinhood listing) that may not repeat simultaneously. A $1.6 billion market cap is already large enough that the multipliers available to early-cycle holders no longer exist — going 100x from here would require a $160 billion market cap, larger than most mid-sized nations’ annual GDP. The ETF filing came and the price went down on news day. Steve Aoki — one of the most visible celebrity crypto holders — sold 4.155 billion $PEPE tokens in April 2026. Insider and early-holder selling into retail attention is the oldest meme coin story.

Both positions are internally consistent. The honest synthesis: $PEPE is a liquid, speculative bet on meme coin narrative cycles at a meaningful discount from its cycle high, with a new institutional catalyst (the ETF) whose impact is uncertain. It’s not a “good investment” in the traditional sense. It is a real, liquid market with specific catalysts and specific risks.

$PEPE Price Prediction 2026

The remainder of 2026 has two distinct phases for $PEPE’s price.

H1 2026 (now through June):$PEPE is bouncing off the $0.000003 support zone. The Canary Capital ETF filing adds a news catalyst that reappears every time the SEC requests more information or issues preliminary guidance. Whale accumulation is active. Meme coin sector sentiment is recovering from the January 2026 highs that had already retraced. The primary resistances to watch: $0.0000041 (50-day EMA approximately), $0.0000055 (short-term bull target cited by on-chain analysts), and $0.000007 (where medium-term recovery becomes significant).

H2 2026 (July through December): If $BTC continues its 2026 trajectory toward new highs and a broad altcoin season materialises, meme coins historically amplify Bitcoin’s moves by 3–5x. $PEPE leading the sector — as it did in January 2026 — would put $0.000010–$0.000015 within reach. An ETF approval decision from the SEC (possible by Q4 2026 if the review runs to its 240-day limit from April 8) would be the single largest potential catalyst in $PEPE’s history after the Binance and Coinbase listings.

The $0.000015 level (roughly a 4x from current prices) is the first significant medium-term target that analysts cite — it would represent approximately half the December 2024 $ATH market cap recovery, achievable in a moderate bull scenario without requiring extraordinary conditions.

$PEPE Price Prediction 2027–2030

The 2030 case for $PEPE is the most straightforward long-term bet in the meme coin category — but only if you accept one premise: that internet meme culture continues to have economic value in the crypto market and that $PEPE specifically retains its position as the dominant expression of that value.

Both premises are contestable. The meme coin space has seen rapid turnover — Dogecoin was dominant in 2021, $PEPE became dominant in 2023–2024, and Solana-based meme coins captured significant attention in 2024–2025. By 2030, there may be three generations of meme coins beyond $PEPE that claim the cultural relevance crown.

But $PEPE’s specific advantages may prove more durable than a single cycle suggests. The Pepe the Frog character is a 20-year-old internet meme — older than most crypto traders’ awareness of crypto itself. Its cultural rootedness predates $PEPE the coin by 18 years. The token has survived two full bear cycles. Its tokenomics — near-complete circulating supply, no ongoing inflation, LP burned — mean the structural supply characteristics don’t get worse over time. The AI-driven content and culture economy of 2026 continues to produce memes at machine speed, keeping frog content in circulation across every major platform.

If $PEPE reaches its 2024 $ATH again by 2030 — roughly $0.000028 — that’s approximately a 7x from current prices, implying a market cap of ~$12 billion. That’s achievable if two to three crypto market cycles occur in the next four years and $PEPE participates in at least one of them at scale.

If the $PEPE ETF is approved and attracts even $1–2 billion in regulated assets, that alone would represent a structural demand floor that $PEPE has never had before.

The extreme 2030 bull case — $0.0001 per token — implies a market cap of ~$42 billion. That would make $PEPE a top-10 cryptocurrency by market cap, larger than projects like Solana at cycle peaks. It’s a theoretical upper bound, not a central case.

Is $PEPE a Good Investment in 2026?

The official $PEPE website already answered this question: the project has “no intrinsic value and no expectations of financial returns.”

That’s honest. It’s also incomplete as an analysis tool.

At $1.6 billion market cap, $PEPE is not a lottery ticket. It’s a liquid, actively traded asset with genuine exchange depth. The question isn’t whether it’s “fundamentally” valuable — it isn’t, by its own admission. The question is whether the market continues to assign it value, and why.

BCR’s analysis of $PEPE’s position in the meme sector identified it as the “cornerstone asset” of the meme category — the one that retail and institutional traders enter and exit most easily when the narrative cycles on. That liquidity premium is real. When meme season arrives, capital flows to $PEPE first because it’s the most accessible entry point, then from $PEPE into smaller names with more explosive upside. $PEPE being 86% below its $ATH with that ETF catalyst in review and that liquidity base intact is genuinely different from $PEPE at its $ATH.

For investors who understand that they’re buying narrative exposure, not earnings, and who can stomach the volatility, $PEPE at current prices offers the closest thing the meme coin sector has to a “value” entry point — relative to its own history.

The ETF is the wildcard nobody had in the previous cycle. If approved, $PEPE becomes accessible to retirement accounts, brokerage accounts, and institutional allocators who can’t touch unregulated crypto directly. The potential size of that demand shift dwarfs anything that drove $PEPE’s prior ATHs.

Bitcoin’s trajectory remains the macro frame for everything $PEPE does. And the evolving DeFi and stablecoin ecosystem of 2026 continues to build the liquidity infrastructure that meme coins parasitise during bull cycles — more DeFi liquidity means more capital available for speculative rotation, and meme coins are speculative rotation’s most reliable destination.

None of that guarantees gains. But it does suggest the conditions for $PEPE recovery are forming, even if the timing isn’t precise.

A week after its newest batch of episodes put the show in second place on Nielsen’s streaming charts, Tyler Perry’s Beauty in Black moved into the top overall spot.

The Netflix drama recorded 1.36 billion minutes of viewing for the week of March 23-29. That’s down a little from 1.42 billion minutes the prior week, but with overall streaming volume down week to week, the small decline was enough for Beauty in Black to move up a place.

The Pitt (1.21 billion minutes) essentially tied its all-time weekly high for the week of season two’s 12th hour. Taking it out one more decimal place, the HBO Max series had 1.208 billion minutes, just shy of the 1.209 billion for the week of Jan. 26-Feb. 1. Beauty in Black and The Pitt were the only titles to cross the billion-minute mark for the week as the previous week’s leader, Virgin River, fell 39 percent to 970 million minutes of watch time.

Hulu’s Paradise (639 million minutes) returned to the original series chart after falling off a week earlier. Something Very Bad Is Going to Happen had a fairly modest opening for Netflix; the series, executive produced (but not created) by Matt and Ross Duffer of Stranger Things fame, came in at 486 million viewing minutes.

Also of note: Peaky Blinders (449 million minutes) charted for the first time since 2022 as the show’s finale movie, Peaky Blinders: The Immortal Man (292 million minutes), debuted on Netflix.

Nielsen’s streaming ratings cover viewing on TV sets only and don’t include minutes watched on computers or mobile devices. The ratings only measure U.S. audiences. The top streaming titles for March 23-29, 2026, are below.

Jaafar Jackson’s portrayal of his uncle Michael Jackson in the eponymous Michael will assuredly be a talking point among the film’s viewers for months ahead, as the younger Jackson delivers an impressive, spot-on take on the King of Pop, from his look to his mannerisms, smile, dance moves — and yes — his voice.

Regarding the speaking voices, that’s all Jaafar and Juliano Valdi, who portrayed a 10-year-old, Jackson 5-era Michael in an equally convincing performance. But getting Jackson’s iconic singing vocals requires savvy sound editing, with the team blending Jaafar and Valdi’s live vocals that they performed on set with Michael’s original recordings.

The actors’ voices are heard in the singing performances when there isn’t a genuine Jackson recording, such as scenes where Jaafar scats in the studio while recording “Don’t Stop Til You Get Enough” or when Valdi does the initial takes of “I Want You Back.” Michael’s voice becomes more dominant when the pure recording is allowed to take over.

“We had the discussion a lot, could we have Jaafar and Juliano go to a studio and record those songs, and the answer was yes,” says Michael music supervisor John Warhurst. “They were capable of delivering those vocals. But then it becomes more an overall philosophy of when people go see the movie, do they want real Michael to be a part of this movie, or do they want it to just be 100 percent Giuliano and Jaafar? Every movie is different, but here we think people want Michael to be a part of it.”

Warhurst has worked on several of the most prominent music films of the past decade, including Bob Marley: One Love, Whitney Houston: I Wanna Dance With Somebody and Bohemian Rhapsody, the latter of which earned him an Oscar. Below, he breaks down the extensive process on how Michael handled the vocals.

Let’s start from the top. How did you guys actually do it?

I’ve worked on quite a few musical films over the years, there’s a few different ways you can approach the vocals. But the best way I’ve found is to approach it like a live musical. That entails the the actor going on set and performing the pieces themselves. Ignore how we’re going to put it together in post-production at this stage. When you use recordings, one of the first things you need is what I call the visual canvas. You can’t put an incredibly powerful voice on a face that doesn’t look like it’s projecting that kind of power. The actors need to learn the songs so that they can actually sing them with the same sort of energy and power as the original artist and then perform it.

Often with these scenes, we’re pretending that we’re in a recording studio, and that means we can actually record. The actor’s wearing headphones. We have a huge microphone in front of them. We should be able to shoot it exactly as if we were recording it for an album. The next important ingredient is as many live takes as you can get without music on it.

It’s more complicated when we do the stadium performances. It isn’t as much like a recording session. There’s more outside of the recording. You see Jaafar doing more of his own bits and pieces and ad libs. And when you’ve got a set that size, you need to really sort of vibe it up a lot. You want the ground to shake. You want everybody to feel it in the room, and it to be that sort of atmosphere.

It sounds like you’re essentially getting stems of their vocals.

Yeah, of their performance. Once we’ve got that right visual canvas and the recordings, when you get to post-production, we’ve got 15 to 20 takes of Jaafar or or Juliano and the one take of Michael with his recording. That’s where the blend comes into it. In that scene when Jaafar is performing as Michael recording “Don’t Stop ‘Til You Get Enough,” he does that scatting stuff. I call that “dialog.” We don’t have Michael doing that. That is Jaafar.

Or that scene of Juliano doing the opening lines of “I Want You Back” where Berry Gordy has to stop Michael and tell him he’s moving too much. If we used Michael on the first take, when we use him again on the final, it’d feel like a carbon copy. So the first time is just Juliano, then the second time when it’s meant to be getting closer we add in some Michael.

How long does the process take?

The process starts as soon as someone gets cast. Especially when it comes to singing, the one thing my ear always picks up on straight away is the strength of voice, in the strength of the vocal, and that’s not something you’re going to do in two or three weeks. You need a lot of vocal coaching.

And then there’s always back and forth in post production, it’s never version one of a movie. Everybody wants to try everything in every single different way possible. You’re constantly reworking. And then you get really happy with the vocal, and they say, “no, we’re going to re-edit this scene.”

How similar a process was it with Bohemian Rhapsody? I know the vocalist Marc Martel was very involved there to get Freddie’s vocals.

It was a very similar process [to get the visual canvas]. The difference with Freddie and Rami was that Freddie was a tenor, and Rami more of a baritone, he had a much deeper voice. That’s where Mark Martel came into it. We understood the differences, and he sounded like Freddie and we could get the vocal if we didn’t have an original recording that fit.

With Jaafar and Juliano, we did not need that. They were both so close. Jaafar is Michael’s nephew. Physically his voice is very close in range and sound to Michael’s, which made my job much easier. In post-production we had several conversations about whether we could just use Jaafar and Juliano or if we needed Michael. They were so close, they nailed it. We ended up deciding it made more sense to keep with Michael. It kept it more consistent across scenes.

If we’re to break down the DNA if you will, particularly with the final product, it sounds like it’s mainly Michael’s vocal, and then Jaafar and Juliano are the anchors to attach the vocal to.

I think of it as the other way around. It’s their performances, with Michael over the top of it.

And to be clear, there’s no AI?

No, I’m very much an audio purist. Once you have the best recording you possibly can, you do the fewest amount of steps away from that record. We apply like EQ, and then we apply compression, and then we apply reverb, and then we stretch it. Those AI tools are amazing but there are bits that are good and then all of a sudden it can sound chewed up.

Working with these actor vocals is obviously a lot more work than lip syncing. How much harder is it to let the actors just lip sync instead?

There is no one in the world who could do it so good, so tight that you wouldn’t detect something when you see it on the big screen. You would feel a slight discrepancy between the image and the sound. People also forget this when you’re on set, we’re not just doing this song once. We’re going all day, and that’s exhausting.

When Michael was on tour, he would go on set that night and sing the song once. We’re going to sing it 24 times for every different angle we could possibly shoot it from. We have to keep that intensity that you see on stage during that first take. When you lip sync, what tends to happen is that is the visual performance drops down as well. It tends to turn into a bit of a goldfish, where the face looks like they’re miming as well. You lose the visual part, and then it just doesn’t work.

Round 1 foes Scottie Barnes and Evan Mobley can’t escape comparisons, or expectations.

Editor’s Note: Read more NBA coverage from The Athletic here. The views on this page do not necessarily reflect the views of the NBA or its teams.

***

TORONTO — It took LeVelle Moten only a few moments to understand Evan Mobley’s greatness. He just had to walk into Team USA’s training camp ahead of the 2019 Under-19 World Cup and watch Mobley work, even as he was coming back from a knee injury.

“I said, ‘That’s what it had to look like when Wilt (Chamberlain) played,’” said Moten, an assistant coach on that team, recalling the camp in Colorado Springs, Colo. “That’s how dominant he was.”

It took until the final game of the tournament for Moten to fully appreciate Scottie Barnes. Moten had put together the game plan, which included a note to not let Mali’s Abdoul Coulibaly go to his left. The starters didn’t follow instruction, so Barnes, who had offered to come off the bench in training camp, got the next crack at the assignment. Barnes immediately let Coulibaly go left, but knocked the ball out of bounds.

“I yelled at Scottie, ‘Damn it, didn’t I say (to) make the boy go left?’” Moten recalled. “And Scottie said, ‘Coach, don’t even worry about it, because this MFer ain’t gonna score no more.’ And he was talking to me — but he was saying it right in the boy’s face.”

The Americans ended up winning Barnes’ 29 minutes by 27 points in a 14-point win, securing the gold medal. Even on a team with the first five picks of the 2021 NBA Draft, plus Tyrese Haliburton, Mobley and Barnes’ gifts could not be hidden. It’s important to remember that, as they continue to nose in front of each other during their intertwined careers, including in the first-round series between their Cleveland Cavaliers and Toronto Raptors, these were hyped-up players who stood out on All-Star teams of their peers. That they exist on the periphery of the NBA’s power structure shows you how special you have to be to get to the inter sanctum of the league’s transactional machinations.

Even in this series, they have not been the fulcrums, as Cleveland guards Donovan Mitchell (62 points, including 8 3s) and James Harden (50 points and 14 assists) have orchestrated a Cavaliers attack that the Raptors have been unable to stop. Most of Cleveland’s defensive attention, meanwhile, has gone toward slowing Brandon Ingram, not Barnes.

But Mobley has been a key cog in the Cavaliers taking a 2-0 lead, with Game 3 going on Thursday in Toronto. When the Raptors benched starting big man Jakob Poeltl and went to a smaller, switch-heavy lineup in the second half of Game 2, Mobley dominated. He had 11 points in the third quarter alone, using his size advantage to neutralize the Raptors’ swarming, pesky defense. He’s averaging 21 points on 77.3 percent shooting through two games.

Calf strains interrupted Mobley’s season a few times during the regular season, part of the reason the Cavaliers didn’t back up their 64-win season a year ago with another six-month waltz.

“They say development is not linear. It just doesn’t keep going like this,” said Cavaliers coach Kenny Atkinson, miming an undeterred ascent with his arm, before Game 2. “It doesn’t. There are going to be some downs, and I think Evan has kind of got out of that dip and is trending back to improving before our eyes and at the right.”

However, the Raptors didn’t wilt in Game 2, and Barnes was the main reason why. He had 17 points in the second half, and was in the middle of the Raptors finally able to push the pace in transition more frequently, a necessity if the Raptors are to make this a series. On a couple possessions, he went right into Mobley and fellow Cleveland big man Jarrett Allen, pushing them under the basket in the paint for buckets. That type of force is necessary for a limited offensive team.

Barnes’ 12-to-9 assist-to-turnover ratio hasn’t been sharp enough, and puts a spotlight on what he has to address in the offseason — one of his handle or his jumper has to improve measurably — and the Raptors’ overall spacing limitations, exacerbated without injured guard Immanuel Quickley.

Both, though, have highlighted the promise that they have shown since they came into the league. Can they be the beating hearts of championship contenders? That’s a different question, one both franchises will have to grapple with on different timelines.

Their careers, dating back to the draft in 2021, have lined up nicely. Mobley went third in the draft, while Barnes went fourth. Barnes edged out Mobley for Rookie of the Year in one of the closest votes for the award ever. And while Cade Cunningham has surpassed both as the guy from that draft who you’d build a team around, both are clearly good enough to be part of a solid franchise’s foundation. There are times when Barnes has seemed like the better player and others when Mobley has seemed like the bigger difference-maker, but neither has ever put the other way behind him.

That’s the tricky part of all of this, though. Barnes came into the league as the guy surrounded by veterans, joining the Pascal Siakam/Fred VanVleet/OG Anunoby core. One by one, those players left, with the Raptors trying to rebuild more in Barnes’ image: frenetic and versatile.

While Barnes’ journey to being “the guy” in Toronto has been awkward — he seemed to demur from the off-the-court aspects of the role to start, and his on-court attributes are certainly more Pippen than Jordan — his personality screams centerpiece.

“Scottie was boisterous. He was talking. He had some of that leadership ability,” said Bruce Weber, the longtime college coach who was the head coach for that Under-19 team. “Sometimes, it had to be reeled in a bit, but you’d rather have that. I always talk about, ‘Do you want to deal with Tigger or Eeyore?’ You want Tigger on your team, because he has energy and is flying around. The successful guys have that energy. That’s why you knew he’d be pretty good.”

As for Mobley?

“You knew when Scottie came into the building,” Weber said. “Evan could sneak in, even at 6-10, 6-11. He could sneak in quietly, and you wouldn’t even know he’s there.”

Perhaps because Mobley’s game was a bit more polished, the Cavaliers decided to accelerate their build right after his rookie year, trading for Mitchell. At times, Mobley has looked like the perfect emerging co-star for Mitchell, a big man who expanded his offensive game last year while winning Defensive Player of the Year.

This season, there has been some disappointment with his development, especially as his shooting has fallen off from the previous two years. Cleveland is so committed to Mitchell now that if the Cavaliers fail to make it to the conference final, you wonder if they might become impatient with Mobley’s growth and move him for a player more obviously in his prime. There’s a guy who has spent his career in Wisconsin who could be available.

That possibility, although probably slim, is more of a reflection of how precious Mitchell’s peak is to Cleveland than anything Mobley has or hasn’t done.

“I think he develops every single year,” Barnes said of Mobley before the series started. “I think he’s grown more into his body. His physicality when he’s driving the ball, being able to create for himself, and defensively, he has all the intangibles. He has super long arms, athletic, he can switch one through five. He’s great.”

Meanwhile, even though Barnes was already an All-Star in 2024, this was the year he blossomed. His defensive impact reached new heights and should earn him his first All-Defense spot — he finished fifth in Defensive Player of the Year voting. With the Raptors acquiring Brandon Ingram to take over the biggest share of the half-court offence that Barnes is not best suited to manage, his energy in pushing the pace, distributing the ball and playmaking on defence animated the Raptors’ surprise 46-win season.

And yet, with Barnes at the middle of things, there will be questions. How do you build a team when your best player is not your most efficient or talented scorer? That becomes a geometry question, one the Raptors are not close to solving. It was exposed during this season, and continues to be in this series.

“He’s a really good passer,” Atkinson said. “I think he’s the 96th percentile in potential assists. You’ve got to keep your eyes open. When he drives, he’s going to find shooters. I’m really impressed (by) the leap he took this year.”

None of that is to suggest the Raptors will consider moving Barnes any time soon. More likely, transaction by transaction, they will attempt to get closer to a roster that makes sense around him, not that it will be easy because of the Raptors’ other financial commitments. The roster-building mistakes the Raptors have around him, especially the contract extension given to Poeltl before this season that doesn’t kick in until 2027-28, make it possible that the Raptors will get stuck in neutral before they can maximize Barnes’ skills. Those mistakes aren’t Barnes’ fault, but they speak to the trickiness of building around him.

Cleveland’s relationship with Mobley is a little more in question only because of Mitchell’s presence and the increased stakes. Still, generally players who are as good as Mobley don’t go anywhere. The safe call is Mobley will be in Ohio for years to come.

“I would like to say they surprised me, but neither of them has,” Moten said. “Evan is who I thought he would be. Scottie is who I thought he would be. I thought, before they were 28 years old, they would both be First Team All-NBA guys. And they’re certainly on the trajectory of doing that.”

Perhaps. Both will turn just 25 this summer. In theory, they still have some evolution ahead of them. But in a league that is trending toward shorter competitive windows, teams won’t always have the time to see their young players’ futures out — even if those players are as good as Barnes or Mobley. Great young players have never had less time to reach their ceilings.

***

Eric Koreen is a senior writer covering the Raptors and the NBA. Previously, he has written for the National Post, Canadian Press, Sportsnet and Complex.