US banks “reduced” their credit risk after 2008 by shifting more of it to nonbank lenders.

Since 2008, banks have shifted a growing share of their lending to nonbanks like private credit funds, making it their fastest-growing loan category.

That shift doesn’t signal another 2008-style crisis today, but it does show where trouble could surface first if private credit starts to crack.

This week, traders, analysts, and Investment firms are reviving a familiar question: are US banks setting up a repeat of 2008?

The clean answer is no, based on the publicly available numbers. The same debate also points to a real shift in bank balance sheets that deserves a harder look.

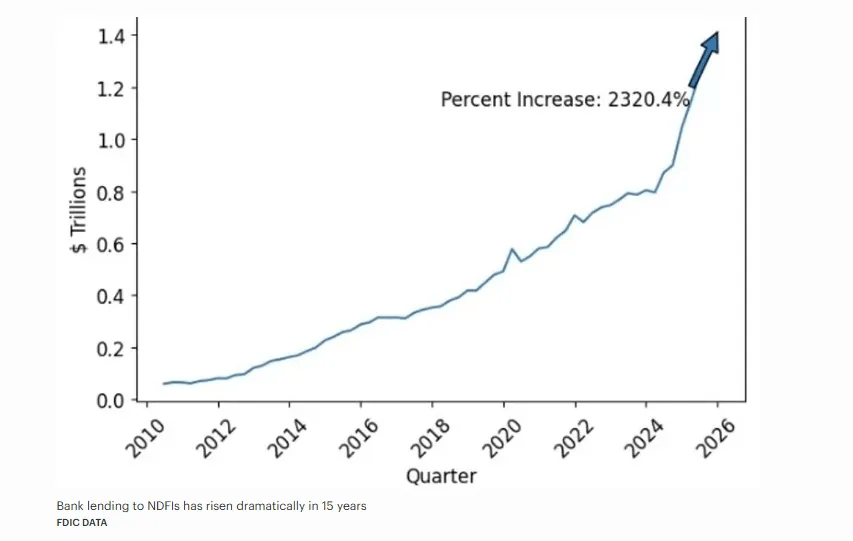

The chart below, which is circulating on X, shows that bank lending to nondepository financial institutions, or NDFIs, rose 2,320% over 15 years.

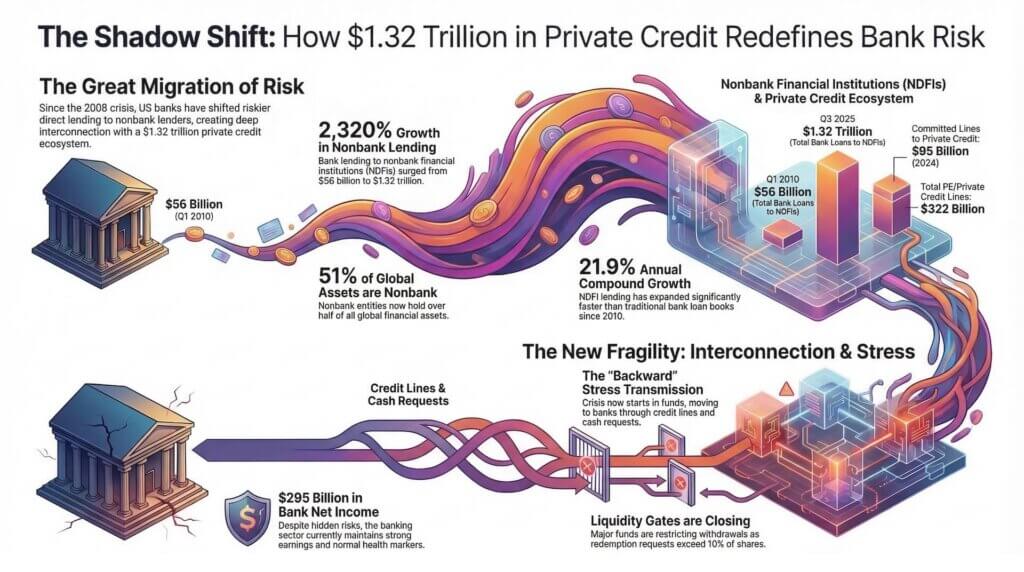

An FDIC note documented $1.32 trillion of those loans by the third quarter of 2025, up from $56 billion in the first quarter of 2010, and called the category the fastest-growing loan segment since the 2008-09 crisis.

After 2008, large banks pulled back from riskier direct lending, but they also funded the nonbank lenders that stepped in. That group includes private credit vehicles, mortgage finance firms, securitization structures, and other parts of the shadow banking system. The risk moved elsewhere rather than disappearing.

However, that does not mean banks are already in trouble. The FDIC’s latest industry profile showed the banking sector earned $295 billion in 2025, posted a fourth-quarter return on assets of 1.24%, reduced unrealized securities losses to $306 billion, and counted 60 problem banks, still within the agency’s normal non-crisis range. Those are not the numbers of a system already in a panic.

The issue is where losses, redemptions, and liquidity pressure land when the lending chain has more links.

For crypto, that changes the timing of any stress. A classic bank panic starts at the bank. In the current structure, stress can begin in a fund, a warehouse line, or a financing vehicle, then work backward into banks if marks fall, borrowers miss payments, or investors ask for cash faster than the assets can be sold.

The post-crisis shift is now visible in the numbers

The official numbers make the structural change hard to dismiss. The FDIC said bank lending to NDFIs compounded at 21.9% a year from 2010 to 2024.

By the third quarter of 2025, the total had reached $1.32 trillion, or roughly 10% of bank lending in the agency’s analysis.

Not every dollar in that bucket is private credit, and exposures in the category carry different levels of risk. Even so, the scale shows that a large share of credit intermediation now sits in institutions that do not take deposits and often disclose less than banks do.

That nuance is important. NDFI is a broad label. It can include mortgage intermediaries, consumer finance firms, securitization vehicles, private equity funds, and other nonbank lenders, alongside private-credit funds.

A sloppy reading turns the whole bucket into one bet on private credit. A more accurate reading is that banks built a large, fast-growing set of links to the broader nonbank system.

Private credit is one visible part of that system, and one of the most closely watched because it grew during a long period of higher rates, tighter bank regulation, and steady investor demand for yield.

A Federal Reserve staff note sharpens this point. It is estimated that committed credit lines from the largest US banks to private-credit vehicles rose from about $8 billion in the first quarter of 2013 to about $95 billion by the fourth quarter of 2024, with roughly $56 billion already drawn.

The same work put total committed bank lines to private credit and private equity at about $322 billion.

That does not prove systemic failure is close. The Fed’s own conclusion was more restrained: direct financial-stability risk from this channel looked limited so far because the largest banks appeared able to absorb major drawdowns.

Even so, growing links between banks and private-credit vehicles warrant close attention.

The risk is best framed as continued bank funding for parts of the lending chain, which changes where stress appears first.

In the public market, losses print quickly. In private markets, they can move more slowly because marks update less often, assets are less liquid, and investor withdrawals are managed through product rules.

That delay can make the system look calm until cash needs force a sharper repricing.

Global context points in the same direction. The Financial Stability Board said the nonbank financial intermediation sector accounted for about 51% of total global financial assets in 2024 and continued to grow at roughly twice the pace of banking, according to its latest report.

This is no longer a US edge case. Credit has been moving into institutions outside the classic banking model for years, and the US private-credit boom is part of that wider pattern.

Why the trade is getting tested now

The issue became more urgent as structural data arrived while private credit began to show public strain. Some private-credit vehicles have limited or managed withdrawals, while JPMorgan tightened some lending against private-credit portfolios after markdowns.

Those events stop short of establishing a full-market break and instead show where pressure is likely to emerge first: fund liquidity, financing terms, and collateral values.

That is also why any comparison to 2008 needs restraint.

The same FDIC report that drove renewed attention also showed banks entering this phase from a stronger income position than during past crises. The public banking system is not in free fall.

The greater concern is a funding architecture that could transmit stress from nonbank lenders back into banks if private assets keep repricing lower or if investors want cash before loans can be sold or refinanced.

Borrower quality and refinancing deserve more attention than broad slogans. In a recent Financial Times interview, Partners Group’s chair said that private-credit default rates could double from their roughly 2.6% historical average over the coming years. That is not an official baseline, and it should not be treated as one.

It does, however, capture the key pressure point. A system built on long-duration private loans, slower marks, and regular financing lines can look stable until defaults rise and refinancing windows narrow at the same time.

For Bitcoin, the setup is awkward in the short run and cleaner in the medium run. At the time of writing, $BTC traded near $73,777 and held 58.5% market dominance, with gains of 0.05% over 24 hours, 4.55% over seven days, and 7.51% over 30 days, according to CryptoSlate data.

That price action suggests crypto is not trading as if a banking event is already underway. If a broader credit squeeze did hit, the first move would likely be a selloff in liquid assets, and Bitcoin is still one of the most liquid assets in global markets.

Over a longer horizon, if the debate broadens into a deeper loss of trust in how the financial system carries leverage and values private assets, Bitcoin’s appeal as an asset outside the banking stack becomes easier to articulate.

That second-order effect is the real contagion risk for crypto.

A private-credit strain does not automatically send capital into Bitcoin on day one. It can easily produce the opposite move.

Over time, though, if banks have to pull back, if fund financing gets harder, and if more investors start asking who really owns the credit risk, the case for holding some assets outside that system becomes easier to make. We know that trade. The banking data now place it in a new macro setting.

What to watch in the next round of data

The next phase of this story will likely emerge through three checks: whether more private-credit vehicles limit withdrawals or take larger marks, whether banks keep financing those funds on the same terms, and whether the NDFI loan book continues to expand at anything close to the pace the FDIC documented over the prior decade.

That is where the current debate becomes more concrete than the usual “shadow banking” label. If banks tighten financing to nonbank lenders, middle-market borrowers can feel it quickly through cost and access, even if no household hears the acronym NDFI.

If the funds meet redemptions by selling what they can, public credit can take some of the price discovery that private books avoided. If the funds do not sell and banks keep financing them, the exposure stays in the system longer.

None of those paths requires a repeat of 2008. All of them can still change how credit flows.

Pressure is already showing in all three areas

The direction of travel so far looks like tightening, not collapse.

On withdrawals and marks, semi-liquid private-credit vehicles are restricting cash more aggressively while investors push for fresher valuations.

A recent report said Cliffwater’s flagship corporate lending fund received redemption requests equal to about 14% of shares and met only 7%, while Morgan Stanley’s North Haven fund received requests equal to 10.9% and honored only its 5% cap.

The same report said BlackRock and other vehicles also hit standard quarterly limits, while Apollo moved toward monthly and then daily NAV reporting to answer criticism of stale pricing.

That points to weaker liquidity conditions and stronger investor demand for faster price discovery and greater cash access at the same time.

On bank financing, lenders are getting more selective rather than shutting the door outright.

A separate report said JPMorgan marked down some software-backed private-credit collateral and restricted lending to affected funds, which reduced borrowing capacity and pointed to tougher collateral treatment in weaker pockets of the market.

That stance is not universal. Other coverage said banks were still willing to finance some withdrawal needs. The signal is narrower and more useful: lenders are still in the market, but they are showing less tolerance for weak collateral and more willingness to tighten terms fund by fund.

On balance-sheet growth, the NDFI loan book has already changed behavior without needing to contract outright.

The FDIC’s February 2026 study said bank loans to NDFIs compounded at 21.9% annually from 2010 to 2024 and reached $1.32 trillion by the third quarter of 2025. A category that grew at that pace does not need an outright contraction to reset underwriting.

Slower growth, more frequent markdowns, and tougher financing terms are enough to change redemption behavior, reduce leverage, and make investors less willing to assume that rapid balance-sheet growth can continue alongside benign losses.

The official numbers argue against panic today, but they do not support complacency.

The FDIC’s balance-sheet data show a large post-crisis migration in bank exposures. The Fed’s research shows large banks remain connected to the private-credit complex through financing lines. Global data show nonbank finance has become too large to treat as a side story, and the first public tests of private-credit liquidity are already showing up in the market.

The next stress point may arrive through a route that looks safer in good times because it sits one step away from the bank.

The next useful check is whether fund withdrawals stay contained, whether bank financing stays open, and whether the $1.32 trillion exposure that the FDIC documented keeps rising as private credit faces a harder year.