Bitcoin price moved back above $76,000 on April 20 after a volatile weekend tied to developments in the United States-Iran conflict. The rebound followed a pullback toward $75,000 as traders reacted to renewed pressure in oil markets and fresh uncertainty around diplomacy.

Market attention also shifted after President Donald Trump said a new U.S. deal with Iran would be better than the 2015 nuclear agreement. That statement arrived as the current ceasefire approached its end and doubts remained over the timing of another round of talks. Against that backdrop, Bitcoin continued to trade as a macro-sensitive risk asset, with price moves shaped by oil, geopolitics, and positioning across derivatives markets.

Bitcoin Price Steadies After Weekend Pullback

Bitcoin price held above $76,000 after retreating from a failed move beyond $78,000. The earlier rise marked the asset’s highest level in about ten weeks before momentum faded into the weekend. Traders reduced risk as tensions in the Middle East returned to the forefront and oil markets turned higher again.

The weekend reversal reflected broader caution across global markets. Reports tied to the Strait of Hormuz and renewed friction between Washington and Tehran pushed crude prices back toward the $90 range. That added pressure to inflation expectations and weighed on assets that are sensitive to macro uncertainty, including Bitcoin.

Donald Trump Comments Shift Focus to Diplomacy

Donald Trump said on April 20 that the deal now being negotiated with Iran would be better than the Joint Comprehensive Plan of Action, the 2015 accord he exited in 2018. His remarks came after criticism from Democrats and some nuclear experts who questioned whether a complex agreement could be reached quickly. The comments added a diplomatic angle to a market already focused on oil supply and ceasefire risk.

At the same time, uncertainty around the next round of talks remained in place. Prospects for further negotiations in Pakistan were not clear as the two-week ceasefire neared expiry.

Oil Volatility Keeps Pressure on Risk Assets

Oil remained central to the market reaction. Reuters reported that the war and renewed disruption around Hormuz had helped lift global oil prices, with Brent and WTI both showing sharp gains. Higher energy prices can keep inflation concerns alive, which in turn can affect expectations for monetary policy and weigh on crypto demand.

Bitcoin’s recent trading pattern gave back part of its earlier rally as geopolitical headlines worsened and crude rose again. Even with the recovery above $76,000, traders continued to monitor whether the market could hold support if oil stays elevated and diplomatic progress remains uncertain.

Bitcoin Price Technical Levels

Market structure also pointed to continued volatility. The earlier move above $76,000 had forced out a large amount of bearish positioning, but the weekend retreat triggered another round of liquidations as traders adjusted to the new macro backdrop. Open interest and options positioning around the $75,000 area suggested that Bitcoin could continue to see sharp price swings in the near term.

Technical levels now remain important for the next move. Resistance sits near the upper $79,000 zone, while support was near $73,000 to $75,000.

The SEC is positioning its first year under Paul Atkins as a turning point toward clearer regulation and stronger markets. The SEC Chair described it as a historic year, stating the agency delivered on its promises.

Key Takeaways:

SEC emphasized regulatory clarity as key to stronger U.S. capital markets.

Paul Atkins framed his first year as historic, with a focus on innovation and growth.

NYSE event reinforced policy shift supporting crypto and market competitiveness.

‘It’s Been a Historic First Year as SEC Chairman’

A first anniversary appearance at the New York Stock Exchange (NYSE) highlighted the market impact of U.S. Securities and Exchange Commission (SEC) Chair Paul Atkins’ policy shift. On April 20, the SEC, Atkins, alongside supportive lawmakers and fellow regulators, cast the milestone as reflecting a year shaped by regulatory clarity, stronger U.S. capital markets, and support for innovation, including crypto.

The SEC detailed that Atkins rang the NYSE opening bell to mark his one-year anniversary as chairman. The agency emphasized a shift toward regulatory clarity and a less enforcement-driven approach to crypto and other emerging technologies, while Atkins described the period as a “historic first year” focused on returning the SEC to its core mission of investor protection, orderly markets, and capital formation.

Commodity Futures Trading Commission (CFTC) Chair Mike Selig stated that the SEC had “ended regulation by enforcement” and supported “innovative technologies like crypto,” while pointing to closer coordination between the CFTC and SEC. That signals clearer operating conditions for digital asset firms in the U.S., as policymakers continue emphasizing innovation, competitiveness, and regulatory alignment.

Atkins was sworn in as the SEC’s 34th chairman on April 21, 2025, after President Donald Trump nominated him on Jan. 20, 2025, and the Senate confirmed him on April 9. The role marks Atkins’ return to the agency, where he previously served as an SEC commissioner from 2002 to 2008. During his current tenure, the SEC has signaled a more industry-friendly approach to digital assets through moves including support for its Crypto Task Force, the dismissal of civil enforcement actions against several crypto firms, and a broader push for clearer crypto guidance.

Atkins Ties Crypto to SEC Core Mission

The SEC chairman further stressed: “I promised a new day at the SEC when I came aboard … We’ve made huge progress,” he said, reiterating:

“When I took office 1 year ago, I promised a new day at the SEC. And we’ve delivered.”

“With our agenda to restore regulatory clarity, strengthen competitiveness, and accelerate innovation, we are making sure the U.S. remains the world’s strongest and safest place to invest,” he stated. Those remarks placed crypto within a broader market strategy while linking policy direction to competitiveness and investor safeguards.

Echoing that stance, House Financial Services Committee Republicans said on X that the SEC advanced policy changes aligned with innovation, stronger U.S. capital markets, and investor protection, adding that “Republican members look forward to continue advancing these efforts.”

Dogecoin shows a cup-and-handle pattern and a bullish divergence in the RSI, pointing to a potential breakout above $0.103.

The $TRUMP token expects volatility due to an event at Mar-a-Lago on April 25, while maintaining critical support at $2.77.

Pepe ($PEPE) leads the sector’s momentum with a weekly rise of 7.3%, facing decisive resistance at the $0.00000416 level.

The fourth week of April begins with an average growth of 8% for the memecoins segment; the marked lagging of the main assets suggests an imminent rotation of capital towards the leaders.

Currently, Dogecoin (DOGE) is trading near $0.09482, making sideways movements while the rest experience rallies. This technical understatement, combined with a clear positive divergence in the RSI oscillator, could skyrocket the price by 12% towards $0.115.

The market appears to be calm, but the formation of a “cup and handle” on the daily chart reinforces the analysts’ bullish thesis. If the buying volume passes the $0.095 barrier, it would confirm the start of a massive recovery phase for the largest meme cryptocurrency by capitalization.

Political catalysts and technical breakout structures

On the other hand, the price of the Official Trump ($TRUMP) token stands at $2.83 with a key event scheduled for this April 25. The gala organized for the main holders acts as a fundamental catalyst that has historically driven speculative demand for the asset.

Meanwhile, Pepe ($PEPE) shows an enviable technical setup called a “pattern within a pattern.” The asset is attempting to invalidate a long-term bearish channel by consolidating a handle just below its main resistance in the Fibonacci zone.

If $PEPE manages to close a daily candle above $0.00000416, it would trigger a measured move towards $0.00000526. This advance would represent a return close to 30%, consolidating its position as the asset with the best relative momentum of the analyzed group.

The memecoins market is going through a critical period of technical and fundamental reconfiguration. The combination of high-impact in-person events and signs of bearish exhaustion positions these three tokens as the indisputable protagonists of this weekly session in the crypto ecosystem.

Solana is pulling back into an area that now matters most for the short term trend. One chart shows price testing a micro support zone, while another keeps the bullish case alive as long as $SOL holds above the broader reversal area.

Solana Pullback Tests Key Micro Support Zone

More Crypto Online says Solana is moving toward a micro support zone while a broader wave two correction may still be in play. The chart shows $SOL trading near $83.53 after a pullback from the recent local high, with price now approaching the first key support area around $81.75 to $80.53.

Solana / U.S. Dollar 1 Hour Chart. Source: More Crypto Online on X

That zone matters because it lines up with several retracement levels shown on the chart. The structure suggests this drop could still fit a wave two correction if buyers hold support and price stays above $78.81. The chart marks that level as the deeper invalidation point for the current bullish interpretation.

At the same time, the rebound setup remains incomplete. $SOL has already lost the rising short term support line, which signals weaker momentum. Therefore, traders will likely watch whether price stabilizes inside the marked support band or continues lower toward the high $78 area.

If support holds, the chart leaves room for another move higher after the correction. If $SOL breaks below $78.81, the current wave count would weaken and the broader pullback case would gain more weight.

Solana Reversal Setup Keeps Bulls in Control

BitGuru argues that Solana has shifted from breakdown fears to a cleaner recovery structure. The chart supports that view. It shows $SOL rebounding after the late March decline, then moving into a consolidation phase before breaking higher and pulling back without losing the broader recovery shape.

The key point is support. Price rejected from the recent high near $90.95 and moved back toward the mid range area around $85. However, the chart still shows $SOL holding above the marked reversal zone near $82. As long as that area stays intact, the pullback looks more like a retest inside an uptrend than a fresh bearish breakdown.

The earlier fall from around $93.45 formed the base for this structure. Since then, Solana has built higher lows and pushed into a stronger range. Therefore, the current dip does not yet cancel the bullish case. Instead, it suggests the market is testing whether buyers can defend support after the breakout.

If $SOL holds this zone, the chart keeps the door open for another move toward the recent highs. If support fails, the reversal setup would weaken and the bullish structure would need to be reassessed.

If you are a bank, your core business model is quite elegant. You take people’s money, you pay them zero percent interest on their checking accounts, and you lend that money out to other people at five or seven percent interest. You keep the difference. This is a very good business, and if you have it, you will fight very hard to keep it.

The problem with paying your depositors zero percent is that eventually, someone else will come along and offer to pay them something. When this happens, you have two choices. You can raise your own deposit rates to compete, which costs you money and ruins your business model. Or you can go to the government and ask them to make it illegal for the others to pay interest.

Historically, banks strongly prefer the second option.

A stablecoin is a cryptocurrency pegged to the US dollar. If you give a stablecoin issuer a dollar, they give you a digital token, put your dollar in Treasury bills, and earn about 4%. Historically, stablecoin issuers have kept that yield for themselves. The obvious next step in the evolution of this product is that they share some of the yield with you, so that you will hold their token instead of leaving your money parked elsewhere.

Under $GENIUS, issuers themselves cannot pay yield to holders. The live CLARITY fight is whether affiliated exchanges, distributors, or rewards programs can share those economics with users in ways that are functionally equivalent to interest.

The banks do not care for this.

And so they are calling their senators. Congress has been locked in talks for months over a crypto regulatory framework — the $GENIUS Act last summer for stablecoin issuers, and now the CLARITY Act for everything else, including the question of what stablecoin players can do. Treasury Secretary Scott Bessent has publicly urged the Senate to move forward:

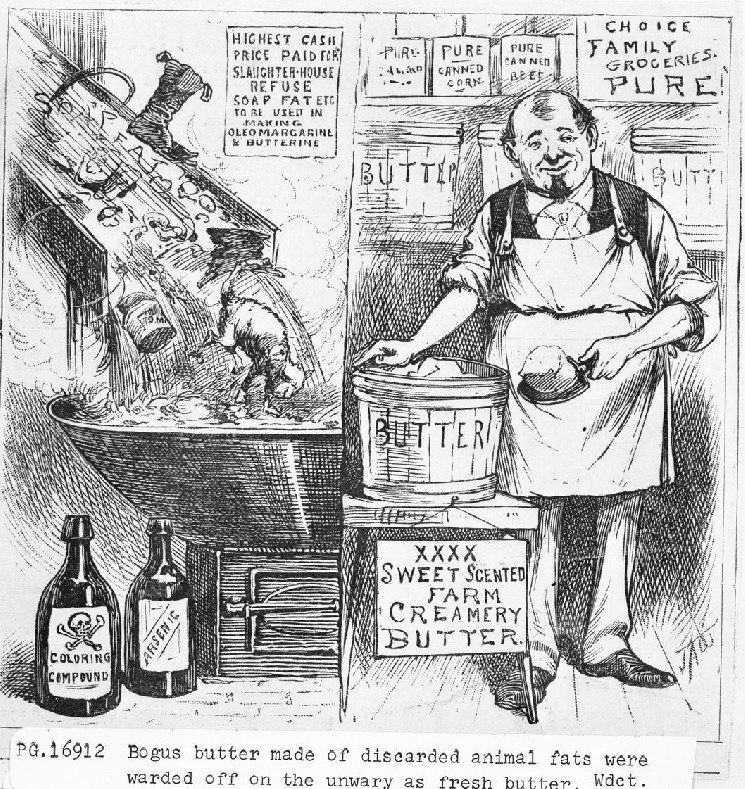

“Bogus butter” was the term used for oleomargarine.

Bettmann Archive

But the traditional banking lobby has demands first. According to Crypto In America reporter Eleanor Terrett, the North Carolina Bankers Association has been circulating a message, encouraging member banks to call lawmakers with this script:

“The CLARITY Act must include an airtight prohibition on payments for stablecoins acting as a store of value by clearly barring any interest or yield-like payments tied to the holding, retention, or balance of payment stablecoins — without carve-outs that can be met through nominal activity or loyalty programs.”

This is a masterpiece of the genre. What the banks are saying, in plain English, is: “We cannot stop stablecoins from existing, but you must legally mandate that they be worse than our products.” They want to ban anything “economically or functionally equivalent” to interest. We are the banks, we own the concept of interest, so you must stop the computer program.

It is also, as it turns out, a margarine law.

In 1869, a French chemist named Hippolyte Mège-Mouriès figured out how to make a cheap spreadable fat from beef tallow. Napoleon III wanted something to feed the army and the poor, and Mège-Mouriès gave him margarine. By the mid-1870s it had arrived in the United States, where it cost significantly less than butter and tasted, to an unaided palate, basically the same. This is the point at which the American dairy industry discovered that it could not compete on price or efficiency with a man who had invented butter in a factory, and so, like all industries that cannot compete on price or efficiency, it turned to the regulators.

By the turn of the century, more than thirty states had passed anti-margarine laws. The pitch was consumer protection: people could not be allowed to accidentally buy margarine while thinking it was butter.

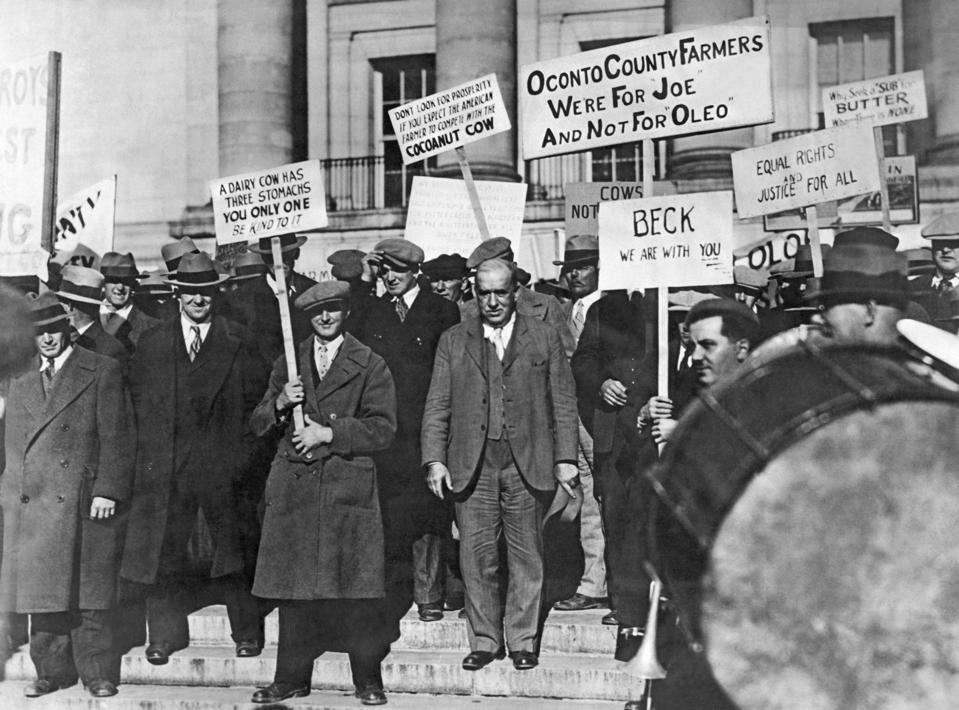

Wisconsin farmers protest the usage and sale of ‘synthetic butter,’ otherwise known as oleo margarine which was made from vegetable or coconut oils, Madison, Wisconsin, circa 1930. (Photo by Underwood Archives/Getty Images)

Getty Images

The mechanism was, in retrospect, spectacular. New Hampshire and Vermont, among others, required margarine to be dyed pink. Not labeled pink. Dyed. The theory was that nobody will spread pink grease on bread, and therefore the product will be technically legal but commercially dead. This is an airtight prohibition without carve-outs that can be met through nominal activity. The Supreme Court struck down New Hampshire’s pink-margarine law in 1898, holding that it was “in necessary effect, prohibitory.”

So the states pivoted. They said: fine, you can sell margarine, but you cannot sell it yellow. Margarine is naturally white. Butter is yellow because cows eat grass. Without the color, the consumer will look at this tub of white grease and reject it. Commercially dead, but this time constitutional. The federal Margarine Act of 1886 added a two-cent-per-pound tax. The Grout Bill of 1902 raised it to ten cents per pound on yellow margarine while leaving uncolored margarine at a quarter of a cent.

Read the Grout Bill carefully. It does tax margarine — but it taxes margarine that resembles butter forty times more heavily. The regulated quantity is not just the product; it is the product’s resemblance to the incumbent product. Substitute “yellow” for “economically or functionally equivalent” and you are reading the March draft of the CLARITY Act.

The margarine industry did what industries do when regulators ban yellow. It shipped the product as a block of white margarine with a separate capsule of yellow dye. The consumer put the block in a bowl at home and worked the dye through with a wooden spoon. Generations of Americans spent the first half of the twentieth century sitting at their kitchen tables, performing a small act of civil disobedience every week to save thirty cents on butter. By the mid-1940s, Leo Peters had patented a plastic pouch with the dye capsule sealed inside, so consumers could pinch and knead the bag instead of mixing margarine in a bowl. This was considered a major innovation. If you are over a certain age, someone in your family may remember this.

Wisconsin kept its yellow-margarine restrictions until 1967, the last state to give up. Minnesota required public disclosure when oleomargarine was served in place of butter. Violations could carry criminal penalties. The point was not subtle: margarine could exist, but the law made restaurants announce the substitution.

Nobody was fooled. Everyone understood the point. The workaround became the product.

Eventually, World War II hit. Butter was heavily rationed, margarine was less so, and American households got so used to mixing the dye that they became much more comfortable substituting margarine for butter. Margarine outsold butter by 1958. The dairy lobby had spent eighty years successfully defending the legal definition of the word “butter,” and in the process had taught an entire country that you could mix your own yellow dye into a cheaper, longer-lasting, identically-functional spread and it would be fine. The carve-out became the industry. By the time Wisconsin gave up in 1967, margarine was not the substitute. It was the mass-market spread, and butter had become the luxury good.

In a strange coda, butter later won a different fight. By the 2000s, margarine’s trans-fat reputation had collapsed, and butter brands increasingly competed on provenance, fat content, and flavor — Irish grass-fed butter, European-style butterfat, cultured butter. The industry that had spent eighty years legislating against its substitute eventually won a different fight, the one no regulator had forced on it, which was to pay attention to what customers actually wanted.

This is the part where you may be nodding and assume the same thing will happen with stablecoins. Which it probably will. But there is a more recent and more financially precise version of this story, and it is even less flattering to the bank lobby, because the bank lobby is the one it happened to.

In 1933, the Banking Act prohibited banks from paying interest on demand deposits and gave the Fed authority to cap rates on savings deposits. This was Regulation Q. It was meant to prevent destructive rate competition and protect the community bank deposit franchise. It was airtight. It had no carve-outs. It was the closest financial ancestor of the regime the NCBA is currently asking Senator Tillis to enact for stablecoins.

In 1971, Bruce Bent and Henry Brown started the first money market mutual fund. It held short-term Treasuries and commercial paper. It passed the yield through to shareholders as “dividends,” because technically it was a 1940 Act registered fund and not a bank. It was functionally a checking account paying market rates, but formally it was a security, and Regulation Q regulated banks, not securities. In 1977 Merrill Lynch added check-writing and a Visa card and called it the Cash Management Account. By the early 1980s, money-market funds had become a $200-billion-plus industry. Today they hold more than $7.6 trillion. Deposit-rate ceilings were dismantled through the 1980s; the demand-deposit interest ban finally disappeared in 2011, seventy-eight years after the original prohibition.

The thing the banks wanted to protect in 1933 — their exclusive franchise over yield-bearing, dollar-denominated, liquid instruments — they lost to a wrapper that was technically not a bank. They did not lose it because of bad regulation. They lost it because the airtight prohibition trained an entire adjacent industry to build the same product in a form the prohibition did not cover.

So. Back to the NCBA sentence.

“Airtight prohibition” is a thing you can ask for. You will sometimes get it. The Oleomargarine Act of 1886 is an airtight prohibition. Regulation Q is an airtight prohibition.

What airtight prohibitions are very bad at is remaining about the thing they were written about. The margarine laws were about butter, until they were about teaching consumers that butter was optional. Regulation Q was about bank deposits, until it was about making money market funds a better savings vehicle for the American middle class. The prohibition works on the dimension the incumbent specified. The industry routes around that dimension. The resulting product is a version of the substitute specifically adapted to the contours of the prohibition. Which tends to make it better.

President Donald Trump signs the $GENIUS Act, a bill that regulates stablecoins, a type of cryptocurrency, in the East Room of the White House, Friday, July 18, 2025, in Washington. (AP Photo/Alex Brandon)

Copyright 2025 The Associated Press. All rights reserved

The CLARITY Act fight is about whether a crypto exchange can pay yield on a stablecoin balance. The banks want airtight. They want no carve-outs met through nominal activity. They want no exceptions for novel loyalty programs or business models. They want an economic equivalence standard strong enough to catch any structure that has the effect of interest, even if it is formally something else. This is, one should grant, a coherent request. It is what a lawyer who understood everything about how margarine beat butter, and everything about how money market funds beat banks, would ask for. It is the prohibition you would draft if you had read the history.

And the reason it will not work is that the airtight prohibition is often the cause of the substitution. It is not the defense against it. The dairy industry did not lose to margarine despite the yellow-dye laws. It lost to margarine because of them. The laws created a product category — mix-your-own margarine — that consumers engaged with at their kitchen tables for fifty years. Regulation Q did not fail to protect banks from money market funds. Regulation Q was the reason money market funds existed in that form.

If the CLARITY Act passes with an airtight prohibition on anything economically equivalent to interest, the stablecoin industry will spend the next decade designing products that are formally something else. They will hand users a white stablecoin and a digital packet of yellow dye and let them mix the yield in at home — which is to say, they will build products specifically adapted to the contours of whatever the government agencies will jointly write in their rulemaking. And at the end of the decade, the bank deposit franchise will discover it has been competing not with stablecoin yield, which is easy to regulate, but with whatever the industry built instead.

A customer enters a Blockbuster store in Dallas, Texas, U.S., on Wednesday, Dec. 4, 2013. Blockbuster announced at the beginning of November that it would be closing all stores as well as ending domestic retail and DVD by mail services. Photographer: Mike Fuentes/Bloomberg

The deeper problem for the banks is that yield is not a side feature they’re defending. Their profit depends on paying depositors zero and earning five, and stablecoins-that-share-yield is specifically the product that breaks that model. This is Blockbuster and Netflix. In 2000, Blockbuster collected $800 million in late fees, which was sixteen percent of its revenue. The company was profitable because it was annoying. The famous story is that Reed Hastings started Netflix because Blockbuster charged him $40 for returning Apollo 13 late; Marc Randolph, his co-founder, has since admitted they made that up because it was the easiest way to explain the subscription model to the press. Which is fine. The story worked because everyone instantly understood what Netflix was selling. They were selling not-Blockbuster. That same year, Blockbuster had the chance to buy Netflix for $50 million and laughed them out of the room. In 2005, it tried to scrap late fees to compete. It could not figure out how to make money without them. It brought them back under a different name and filed for bankruptcy in 2010. The airtight prohibition is the version of that story where Blockbuster gets Congress to ban flat-rate subscriptions. Which is, in effect, what the banks are asking for.

NEW YORK – MARCH 17: People stand inside the offices of JP Morgan Chase on March 17, 2008 in New York City. (Photo by Michael Nagle/Getty Images)

Getty Images

Not every bank is Blockbuster. The smart response to better rails is to use the better rails. JPMorgan has done exactly that: its deposit token JPMD — which can pay interest because it is a bank deposit rather than a stablecoin — launched on a public blockchain last year. Multiple banks are running similar tokenized-deposit products on their own private blockchains, which is a permutation of the same bet. The largest banks are not sitting this one out. They are building the product the NCBA wants Congress to ban. Which suggests the lobbying is less a strategy than a delay tactic — one that won’t save the banks running it, because the loudest banks in the lobbying fight may not be the banks best positioned to compete.

The White House Council of Economic Advisers published a paper two weeks ago arguing that a complete ban on stablecoin yield would increase aggregate bank lending by $2.1 billion — 0.02 percent of total loans. The American Bankers Association rebutted this by saying the CEA had studied the wrong question. On this one narrow point, the ABA is right. The CEA studied the current-scale lending effect of a prohibition. The relevant question is what happens in year twenty. The relevant comparison is not money market funds in 1972. It is money market funds in 2011.

The banks are welcome to get the airtight prohibition they are asking for. They should probably be careful what they ask for. The last time they asked for one, they got Vanguard. The time before that, somebody got Wisconsin.

Ethereum derivatives experienced two synchronized liquidation waves in April, driven mainly by long position unwinds across major exchanges.

Open interest dropped sharply on Gate.io (-$840M) and Binance (-$205M) during peak pressure.

Despite volatility, funding rates and taker ratio recovered to neutral levels, showing the market absorbed leverage efficiently without structural breakdown.

Ethereum derivatives went through two major liquidation events in April, marked by a sharp reduction in open interest across leading exchanges. The pressure was concentrated on Gate.io and Binance, where leveraged positions built during the early-month rally were rapidly unwound. Even with the size of the deleveraging, $ETH price remained relatively stable, reflecting efficient absorption of risk.

Ethereum Derivatives See Two Major Liquidation Events in April Market Remains Resilient

On April 18, open interest fell sharply. Gate.io recorded a drop of about $840 million, while Binance lost $205 million in the same session. A second wave followed shortly after, reinforcing that leverage had rebuilt too fast after an earlier correction. $ETH traded near $2,425, where speculative positioning had expanded.

Earlier in April, between April 2 and April 5, a smaller liquidation cycle also occurred. That initial flush reduced leverage briefly, but open interest rebuilt quickly, setting up the second, larger unwind.

Leverage Flush And Funding Rate Signals

Funding data showed pressure concentrated on long positions. Binance funding fell to -0.0045%, indicating crowded longs paying to maintain exposure during the decline. This reflects long liquidation rather than short squeeze conditions.

Across exchanges, funding moved to neutral or negative levels, confirming longs were being forced out rather than shorts covering. The selloff accelerated as liquidations turned into market sell orders.

Taker Ratio Recovery And Market Positioning

The taker buy/sell ratio dropped to 0.916, then recovered to 1.013. This rebound signals that immediate selling pressure has eased and the market has stabilized.

In a broader context, 1.013 is neutral. Historically, stronger $ETH rallies align with levels above 1.05, while sustained weakness appears below 0.93. Current data shows balance rather than conviction.

Open interest has returned close to early-April levels, indicating excess leverage has been cleared. Funding has normalized, reducing fragility.

In conclusion, Ethereum derivatives saw two leverage resets in April without structural damage. The market is now cleaner, and the next move depends on whether spot demand absorbs renewed positioning or leverage rebuilds too quickly again.

John Oliver, host of HBO’s Last Week Tonight, targeted prediction market platforms on his show’s latest weekly deep dive.

In Sunday’s airing of the HBO show, Oliver discussed some of the trivial event contracts on platforms such as Kalshi and Polymarket, including betting whether members of the Trump administration would use certain words in public addresses, to the companies’ controversial partnering with news organizations.

Specifically, the host questioned Donald Trump Jr.’s relationship with both platforms — an adviser to Kalshi and Polymarket — and how the US Commodity Futures Trading Commission (CFTC) “doesn’t even seem to be trying” to block event contracts on terrorism, assassination and war under Chair Michael Selig.

For much of the show, Oliver discussed how it is “incredibly easy for individuals to manipulate the outcomes,” citing Coinbase CEO Brian Armstrong rattling off a list of crypto-related words in his third-quarter 2025 earnings call to cause many Kalshi and Polymarket users to win their bets.

“I’m going to make you a promise tonight,” said Oliver, echoing Armstrong’s statement. “I will never do anything because someone online placed a bet on it. So you can be confident that if I ever say Bitcoin, Ethereum, blockchain, staking and Web3, it won’t be because I’m trying to move markets — it will be because I’m having a stroke.”

Source: HBO Last Week Tonight

While user activity and trading volume on prediction markets have increased exponentially in recent months — expected to reach $1 trillion by 2030 — the platforms’ controversial bets and legal status in US states have raised eyebrows for some experts. Gaming authorities in several states are suing companies like Kalshi over alleged illegal sports betting, with Coinbase chief legal officer Paul Grewal and others expecting the legal fight to end up before the US Supreme Court.

Related: Senate bill to target sports betting ban on prediction markets: WSJ

Financial giants looking to expand into prediction markets?

In addition to previously announced partnerships with media giants like CNN, CNBC, Fox News and Dow Jones, traditional financial companies including Charles Schwab and Citadel Securities recently signaled plans to consider prediction markets.

Charles Schwab CEO Rick Wurster said on a Thursday investors call that the company would “take a hard look at” prediction markets. In a separate event the same day, Citadel Securities President Jim Esposito said that the company was “absolutely keeping an eye on developments” as part of a potential move into the market.

Magazine: Adam Back says current demand is ‘almost’ enough to send Bitcoin to $1M

Bitcoin is showing renewed strength after a sharp rebound, signaling that buyers are stepping back in at key levels. With momentum building and price pushing higher, attention is now shifting toward the $79,000 resistance zone, where a breakout could confirm continued upside and open the door for a stronger rally.

Selling Pressure After Initial Reaction

Bitcoin saw an immediate response to yesterday’s developments, facing notable selling pressure as the market processed the news. Analyst Kamile Uray highlights that while the initial reaction was bearish, the possibility for a continued rally remains on the table, provided the immediate low of $73,371 is successfully defended.

However, a 4-hour candle close below this mark would likely trigger a deeper correction toward the $68,720 level, which represents the critical 0.618 Fibonacci retracement of the most recent upward wave. Holding this support provides the foundation for a fresh leg up.

Source: Chart from Kamile Uray on X

On the bullish side, a decisive close above $79,000 would signal a continuation of the broader uptrend toward much higher targets. Uray identifies a major resistance cluster between $98,000 and $107,000–$109,000. Should the price face a rejection at these elevated levels, traders should expect a return to the previous support zones, ranging from $73,371 to the $66,000 region.

Examining the daily timeframe, the $65,666 level serves as a pivot point. As long as Bitcoin maintains its position above this threshold, the overall structure remains skewed toward a potential rise.

A failure to hold the $65,666 level would shift the focus to lower support levels at $63,823, $62,433, and $60,000. The most critical warning comes at the $60,000 mark; a daily close below this psychological and technical barrier would likely extend the corrective phase significantly.

Bitcoin Bounces Strongly As Week Kicks Off

In his most recent update, analyst Michaël van de Poppe noted a relatively strong upward bounce for Bitcoin on Monday. This movement is particularly significant as it occurs during a period where markets typically trend toward a risk-off stance ahead of the weekly opening. The ability of Bitcoin to push higher against this cautious backdrop suggests underlying strength in current demand.

A key factor in this analysis is the recent decoupling from traditional safe-haven assets. While Bitcoin has shown resilience and upward momentum, gold has trended downward. Looking at the weekly outlook, the presence of a price gap at the $77,300 level remains a primary focal point for traders. Given the strength of the recent bounce and the existing technical vacuum toward that higher level, Bitcoin is expected to fill this gap and achieve new highs before the current week concludes.

$BTC trading at $75,130 on the 1D chart | Source: BTCUSDT on Tradingview.com

In a significant move for the digital asset ecosystem, blockchain tracking service Whale Alert reported on April 2, 2025, that a colossal 301 million $PYUSD—PayPal’s dollar-pegged stablecoin—was permanently burned from circulation. This event, originating from an unidentified wallet, represents one of the largest single stablecoin burn transactions recorded on the Ethereum blockchain to date, immediately drawing intense scrutiny from market analysts and institutional observers worldwide.

$PYUSD Burned: Unpacking the Transaction Mechanics

Blockchain data confirms the burn transaction occurred at 14:37 UTC. Consequently, the action permanently removed the tokens from the available supply. The burn mechanism is a fundamental cryptographic process. Specifically, it involves sending tokens to a verifiably unspendable address, often called a ‘burn address’ or ‘eater address.’ This address has no known private key. Therefore, any assets sent there become irretrievable. The Ethereum network publicly records and immutably verifies this action.

For context, the total circulating supply of $PYUSD stood at approximately 1.8 billion tokens before this event. As a result, this single burn reduced the total supply by nearly 17%. This percentage is substantial for any major stablecoin. Typically, stablecoin issuers like Paxos, which mints $PYUSD for PayPal, manage supply through minting (creation) and burning (destruction) processes. These processes respond directly to user demand and redemption activity. However, a burn of this magnitude, executed in one transaction, is highly unusual.

Stablecoin Supply Dynamics and Market Impact

The immediate market implication revolves around basic supply and demand economics. A reduced supply of a stablecoin, all else being equal, can theoretically increase its scarcity value. However, $PYUSD maintains a strict 1:1 peg to the US Dollar. Therefore, its market price should remain stable at one dollar. The true impact lies in the on-chain liquidity available for trading, lending, and decentralized finance (DeFi) protocols. Major liquidity pools on platforms like Uniswap and Curve Finance may experience temporary imbalances.

Historically, large stablecoin burns often correlate with decreased trading activity or institutional redemptions. For instance, when Tether (USDT) or USD Coin ($USDC) undergo significant burns, analysts typically interpret it as capital moving off-chain back into traditional banking systems. In this case, the burn could signal several scenarios:

Institutional Redemption: A large holder, or ‘whale,’ may have cashed out a significant position, prompting Paxos to burn the corresponding $PYUSD tokens.

Supply Management: PayPal and Paxos might be proactively managing the supply to align with lower demand or to maintain optimal reserve ratios.

Treasury Operations: The action could be part of internal treasury restructuring or the movement of assets between controlled wallets, with a public burn as the recorded outcome.

Market data following the burn showed no immediate deviation in $PYUSD’s market peg across major exchanges. This stability demonstrates the robustness of the reserve-backed model.

Expert Analysis on Reserve Transparency and Trust

Financial technology experts emphasize that such events test the transparency promises of stablecoin issuers. Paxos, as the issuer, publishes monthly attestation reports from independent accounting firms. These reports verify that the outstanding $PYUSD tokens are fully backed by US dollar deposits, US Treasury bills, and similar cash equivalents. Following a burn of this size, the next monthly attestation will be scrutinized to confirm a corresponding reduction in claimed reserve assets.

Dr. Anya Sharma, a blockchain economist at the Digital Asset Research Institute, notes, ‘A transparent and verifiable burn reinforces the core value proposition of a regulated stablecoin. It demonstrates that the supply contract is functioning as intended—tokens are destroyed when dollars are returned. This action, while large, is a stress test that passed smoothly. The market’s calm response is a positive signal for the maturity of the asset class.’

This event occurs within a broader regulatory context. Furthermore, global standards for stablecoins are evolving rapidly. The European Union’s Markets in Crypto-Assets (MiCA) framework and pending US legislation place strict requirements on reserve management and redemption policies. Proactive supply management through burns may become a standard compliance practice.

Comparative Analysis with Historical Stablecoin Burns

To understand the scale, comparing this event to other major stablecoin adjustments is instructive. The table below highlights significant recorded burns.

As shown, the $PYUSD burn is notable for its high percentage of the total supply. The Binance USD ($BUSD) burns in early 2024 were larger in absolute value but occurred over multiple transactions due to Paxos winding down the token under regulatory guidance. The concentrated nature of this single $PYUSD transaction makes it a unique case study.

Conclusion

The burning of 301 million $PYUSD represents a pivotal moment for PayPal’s stablecoin project. It highlights the active, on-chain management of digital dollar supplies. Moreover, it underscores the responsive mechanisms embedded within regulated stablecoin architectures. For investors and the crypto market, the event passed without disrupting the asset’s peg. This stability reinforces confidence in the underlying technology and reserve models. Ultimately, as stablecoins like $PYUSD mature, transparent supply adjustments through burns will likely become normal operational events. They signal a dynamic market responding to real-world demand and sophisticated treasury management. The focus now shifts to subsequent attestation reports and any potential statements from Paxos or PayPal regarding the rationale behind this substantial supply reduction.

FAQs

Q1: What does it mean to ‘burn’ a stablecoin like $PYUSD? Burning a stablecoin means permanently removing it from circulation by sending it to a cryptographic address from which funds cannot ever be retrieved. This reduces the total supply of the token and is typically done when the issuer redeems the token for its underlying collateral, like US dollars.

Q2: Why would someone burn 301 million $PYUSD? The most likely reason is that a large holder redeemed the tokens for US dollars with the issuer, Paxos. Following the redemption, Paxos would execute the burn to accurately reflect the reduced liability on its balance sheet and maintain the 1:1 reserve backing.

Q3: Does burning $PYUSD affect its price or dollar peg? In a properly functioning system, a burn should not directly affect the market price, which is maintained by arbitrage and redemption mechanisms. The price should remain at $1.00. The burn primarily affects the available on-chain supply for trading and DeFi use.

Q4: Who is responsible for the $PYUSD burn transaction? The transaction was sent from an unidentified wallet. However, the action is almost certainly authorized and executed by Paxos, the regulated issuer of $PYUSD, as part of its treasury and supply management operations following a large redemption.

Q5: How can the public verify that the burned $PYUSD is truly gone? Anyone can verify the transaction on a public Ethereum blockchain explorer like Etherscan. The tokens are sent to a ‘burn address’ (e.g., 0x000…dead). This address is publicly known to have no accessible private key, providing cryptographic proof the assets are permanently locked.

The NSA is deploying Claude Mythos Preview despite the Pentagon—which oversees the agency—designating Anthropic a supply-chain risk in March, per a report.

Anthropic CEO Dario Amodei met with White House Chief of Staff Susie Wiles and Treasury Secretary Scott Bessent on April 17, with both sides calling the discussions “productive.”

An administration source told Axios that every federal agency except the Department of Defense wants access to Anthropic’s AI tools.

The National Security Agency is running Anthropic’s Claude Mythos Preview inside its classified networks, according to two sources cited by Axios—a surprising development given that the NSA falls under the Department of Defense, which declared Anthropic a supply-chain risk in March and is currently fighting the company in federal court.

Claude Mythos is not a standard enterprise tool. When Anthropic unveiled the model earlier this month, it restricted access to a handful of vetted organizations, arguing that the model poses serious offensive security risks. Anthropic’s own technical documentation found that Mythos was able to identify critical vulnerabilities in every widely used operating system and web browser. The company judged it too dangerous for open release.

Most organizations with access are using the model defensively, scanning their own infrastructure for weaknesses before adversaries do. The initiative, branded Project Glasswing, includes Microsoft, Google, Apple, Amazon Web Services, JPMorgan Chase, and Nvidia. What the NSA is doing with Mythos is less clear, though the agency’s mission is not purely defensive. A third source told Axios the model is being used more broadly within the intelligence department.

The Pentagon’s hostility toward Anthropic traces to negotiations that went bad. In July 2025, the two sides signed an agreement making Claude the first frontier AI model cleared for use on classified networks. Talks soured when the Pentagon sought to renegotiate, demanding the military be allowed to use Claude “for all lawful purposes” without restriction. Anthropic refused, drawing two firm lines: no autonomous weapons, and no domestic mass surveillance.

When negotiations collapsed, Defense Secretary Pete Hegseth declared Anthropic a supply-chain risk in late February—an unprecedented designation, and the first ever applied to an American company. A California federal judge blocked the move, but then a D.C. appeals court denied Anthropic’s separate bid to halt the blacklisting while litigation plays out. The two sides remain in court.

While the legal fight grinds on, the rest of the administration is moving in a different direction. On April 17, Anthropic CEO Dario Amodei met with White House Chief of Staff Susie Wiles and Treasury Secretary Scott Bessent. Anthropic described the session as “productive”, Reuters reported. The White House said the parties “discussed opportunities for collaboration, as well as shared approaches and protocols to address the challenges associated with scaling this technology.”

President Trump, asked by reporters about the meeting, said he had “no idea” Amodei had been at the White House, after he previously ordered the administration not to use Anthropic’s “woke” models. Bessent and Federal Reserve Chair Jerome Powell have separately been encouraging major bank CEOs to test Mythos and be prepared for security threats, and an administration source told Axios that every federal agency except the Defense Department wants access to Anthropic’s tools.

The NSA’s reported use of Mythos comes as questions mount about whether the model’s capabilities can be contained at all. Decrypt reported last week that researchers at Vidoc Security reproduced several of Mythos’s most alarming cybersecurity findings using publicly available models—including OpenAI’s GPT-5.4 and Anthropic’s own Claude Opus 4.6—without any special access to Mythos itself.

Anthropic did not immediately respond to a request for comment by Decrypt.

Daily Debrief Newsletter

Start every day with the top news stories right now, plus original features, a podcast, videos and more.