Crypto trading firm and market maker GSR has launched its first exchange traded fund, the GSR Crypto Core3 ETF, giving investors exposure to Bitcoin, Ether, and Solana.

The fund, which trades on Nasdaq under the ticker BESO, uses an actively managed structure, includes staking rewards, and carries a 1.00% management fee, marking GSR’s expansion into the fast growing U.S. digital asset fund market.

The new product marks a notable step for GSR, which has spent years operating as a crypto market maker and liquidity provider and is now pushing further into asset management.

Framework Digital Advisors is serving as the fund’s investment adviser, while GSR is positioning the ETF as a bridge between traditional finance demand and crypto native market expertise.

Core3 allocates across Bitcoin, Ether, and Solana and rebalances weekly using research driven signals aimed at improving returns over time. GSR said the strategy is built around two of the market’s biggest themes, Bitcoin’s role as a macro asset and the continued growth of blockchain networks such as Ethereum and Solana, which support use cases including stablecoins and tokenization.

The launch also reflects how quickly the U.S. crypto ETF market is broadening. GSR’s filing for Core3 had already been part of a wider pipeline of crypto fund proposals that moved beyond single token exposure and into baskets, staking, and active strategies. That expansion accelerated after rule changes in 2025 opened a faster path for plain vanilla crypto exchange traded products, helping fuel a wave of new listings and copycat filings.

Earlier U.S. listed products tied to Solana introduced regulated fund structures that pass through staking rewards, and later market commentary pointed to regulatory clarification around protocol staking as a major catalyst for ETF innovation. BESO now takes that trend a step further by combining staking with a multi asset portfolio and active allocation inside a single listed vehicle.

PCMag.com is a leading authority on technology, delivering lab-based, independent reviews of the

latest

products and services. Our expert industry analysis and practical solutions help you make better

buying

decisions and get more from technology.

Sam Reid plays the camp vampire rock star Lestat de Lioncourt looking to set the record straight after being alive and undead for 265 years in the official trailer for AMC’s The Vampire Lestat drama that dropped on Wednesday.

The Interview With The Vampireseries, based on the late Anne Rice’s Vampire Chronicles books, has been retitled for the third season, as Reid’s character looks to reclaim his centuries-old story as an immortal, yet turbulent rock star.

“It’s my era. I’m a rock star now,” a strutting de Lioncourt says at one point in the stylized and fast-paced teaser trailer, with one camera angle revealing the celebrity touring performer’s boots have the word “Hate” on one sole and “Me” on the other.

But, as he attempts to set the record straight with a “rewrite” of the Vampire Chronicles, de Lioncourt’s life begins to spin out of control as he is haunted by the muses from his rebellious past.

“I’m immortal… I’ve been a monster. This is my reckoning,” Reid’s character cries out as AMC reveals the latest series from its Immortal Universe that in the teaser has Lestat playing his version of Billy Idol’s catchy “Dancing With Myself” track.

Along with Reid, The Vampire Lestat stars Jacob Anderson, Assad Zaman, Bogosian, Delainey Hayles and Jennifer Ehle and is executive produced by Mark Johnson, creator, writer and showrunner Rolin Jones, Hannah Moscovitch, Christopher Rice and Anne Rice.

A new documentary argues that Bitcoin creator Satoshi Nakamoto was two people: late cryptographers Hal Finney and Len Sassaman.

The documentary’s investigation relied on a process of elimination that tapped a Unabomber investigator and cross-referenced suspects’ online activity.

The directors told Decrypt that a 90-minute interview with disgraced crypto mogul Sam Bankman-Fried didn’t make the final cut.

A documentary released on Wednesday asserts that Satoshi Nakamoto was never an individual, but rather a pseudonym shared by two expert cryptographers who combined forces to create Bitcoin before their respective deaths: Hal Finney and Len Sassaman.

Directed by Tucker Tooley and Matthew Miele, “Finding Satoshi” showcases a four-year investigation guided by American business writer William D. Cohan and private investigator Tyler Maroney, delving deep into one of the 21st century’s greatest unsolved mysteries.

The film features well over a dozen interviews, ranging from the wealthiest people in the world to computer scientists who helped uncover Satoshi’s identity, sometimes unintentionally.

Investigations into Satoshi’s identity can bring unwanted legal or personal scrutiny to the individuals—longtime Bitcoin Core developer Peter Todd, for example—yet the conclusion of “Finding Satoshi” provokes little consternation because its suspects are no longer alive.

In some ways, the documentary appears to break new ground, featuring an interview with Fran Finney, the late cryptographer’s widow. In the film, she concedes that her husband probably played a role in Bitcoin’s creation. Cohan told Decrypt, “I think [that] was very, very powerful.”

Sassaman’s widow, Meredith L. Patterson, is also included in the documentary, assessing whether her husband could’ve been Satoshi as well. But that’s not before other suspects are identified first: Adam Back, Nick Szabo, David Chaum, Paul Le Roux, and Wei Dai.

In many ways, the film comes across as a love letter to the digital underground where Satoshi found fertile ground, namely privacy-fighting cypherpunks. Phil Zimmermann is among the most notable featured in the film, a privacy pioneer who armed the public with “military-grade” email encryption in the early ‘90s by creating Pretty Good Privacy (PGP).

Sassaman, who took his own life in 2011 after Satoshi’s final public post, and Finney, who passed away due to complications from ALS in 2014, both worked on PGP’s encryption. The documentary theorizes that Finney composed Bitcoin’s code, while Sassaman handled written matters, including Bitcoin’s foundational nine-page white paper.

Before Cohan and Maroney land on their suspects, Finding Satoshi’s directors devote ample time to mapping out the cultures that Bitcoin was likely born from—such as the Extropians, a group of techno-optimist transhumanists—and various Bitcoin forerunners that Satoshi combined elements of, including Adam Back’s Hashcash.

Back, the co-founder and CEO of Bitcoin infrastructure firm Blockstream who established the concept of proof-of-work, was recently fingered as Satoshi in a New York Times investigation, which leaned heavily on linguistic analysis. Following the article’s publication, Back denied that he was Satoshi, as he has done many times.

“If you had a $100 billion fortune, you’re not just going to sit there and live a life of frugality,” Cohan said, referring to the estimated 1.1 million Bitcoin that Satoshi holds. “We just used our analysis and deductive reasoning to get to a different conclusion.”

The film’s investigators enlisted the help of Kathleen Puckett, a former FBI agent who helped bust Unabomber Theodore John Kaczynski, to assess the motivations of whoever wrote Bitcoin’s white paper. Her analysis: Bitcoin’s creator didn’t seem to care about money.

Back is eventually eliminated alongside several Satoshi candidates following a conversation with Alyssa Blackburn, a data scientist who previously worked at Rice University and Baylor College of Medicine in Houston. She provides Cohan and Maroney with data that allows them to measure suspects’ online history against Satoshi’s. The profile fits Finney and Sassaman.

The flick also presents a fact flagged by Jameson Lopp, CTO of security firm Casa, as a potential counterpoint: Satoshi emailed back and forth with a developer at the same time that Finney, an avid runner, participated in a race in Santa Barbara, California.

That discrepancy ultimately backs investigators’ theory that Finney composed code, while Sassaman composed sentences. Still, Cohan and Maroney said that they conducted plenty of interviews across the cryptosphere that didn’t move the needle much.

Conducted at the height of his powers in 2021, a 90-minute interview with FTX founder and former CEO Sam Bankman-Fried didn’t make the final cut, Cohan said. The disgraced crypto mogul was later sentenced to 25 years in prison for orchestrating a multibillion-dollar fraud scheme.

The documentary features interviews from other figures in finance, including Strategy’s Michael Saylor and Microsoft’s Bill Gates. Cohan noted that those individuals appeared to downplay the importance of Satoshi’s identity, effectively giving investigators a stiff-arm.

“We spent a year and a half interviewing all these people,” Cohan said. “They’re fascinating, and they should be their own separate documentary, but we weren’t getting anywhere.”

Daily Debrief Newsletter

Start every day with the top news stories right now, plus original features, a podcast, videos and more.

Robinhood Ventures Fund I purchased approximately $75 million of OpenAI common stock.

The publicly-traded closed-end fund is intended to democratize access to private markets without accreditation requirements or investment minimums.

The fund’s portfolio includes Stripe, Databricks, ElevenLabs, Ramp, and Revolut alongside its new OpenAI position.

Robinhood Ventures Fund I purchased approximately $75 million of OpenAI common stock, the fund announced Wednesday, letting retail investors who buy shares in Robinhood’s publicly traded fund get exposure to the AI giant.

The investment represents a significant addition to RVI’s concentrated portfolio of high-growth private companies, which includes Airwallex, Boom, Databricks, ElevenLabs, Mercor, Oura, Ramp, Revolut, and Stripe. OpenAI, the maker of ChatGPT recently valued at $852 billion, marks one of the fund’s largest single investments since launch.

“OpenAI is one of the frontier artificial intelligence companies, and we are incredibly proud to add them to the Fund,” said Sarah Pinto, president of Robinhood Ventures Fund I, in a statement. “As one of RVI’s largest investments to date, this underscores our core mission to provide everyday investors with access to what we believe are transformative companies shaping the future.”

RVI’s structure as a closed-end fund enables retail investors to access private company valuations through standard brokerage accounts. The fund eliminates barriers that typically restrict private market investments to wealthy accredited investors, including high minimum thresholds and complex investment structures.

The timing aligns with growing retail interest in AI investments across crypto-adjacent platforms. Robinhood’s push into AI exposure comes as traditional finance and crypto platforms increasingly compete for retail investment dollars in emerging technology sectors. The fund’s public listing allows investors to trade shares like any stock, providing liquidity that direct private investments lack.

The investment highlights a significant shift in market composition, with the number of publicly traded companies in the U.S. falling from 7,000 in 2000 to 4,000 last year. Meanwhile, private companies have grown to outnumber public companies by more than 6.5 times as of April 2024, with the estimated value of private firms surpassing $10 trillion in the first quarter of 2025.

Led by Sam Altman, OpenAI is one of the largest players in the frontier AI space, competing with fellow startup Anthropic—the maker of Claude—and tech giant Google with its Gemini series of models.

Both OpenAI and Anthropic are believed to be laying the groundwork for public offerings, perhaps as soon as later this year. Users on Myriad—a prediction market platform operated by Decrypt‘s parent company, Dastan—currently believe that Anthropic will be the first of the AI giants to go public, penciling in nearly 64% odds as of this writing.

Daily Debrief Newsletter

Start every day with the top news stories right now, plus original features, a podcast, videos and more.

Leonardo DiCaprio is marking Earth Day by calling on his 60 million Instagram followers to contact members of the U.S. House of Representatives and urge them to vote “no” on a bill that seeks to dismantle the Endangered Species Act (ESA), which was signed into law by Richard Nixon in 1973. The ESA is the primary law protecting and conserving species in the U.S. from extinction.

“Today, on Earth Day of all days, the U.S. House of Representatives is set to vote to gut the Endangered Species Act (ESA), trading the future of life on Earth for the short-term economic gain of a wealthy few,” DiCaprio wrote in a statement on Instagram. “The ESA was signed into law over 50 years ago by President Nixon after passing 92-0 in the Senate and 355-4 in the House, ensuring the safeguarding of species and ecosystems that sustain us. Today’s bill would devastate the most vulnerable species, which are essential to functioning ecosystems.”

“I urge the House to reject this existential threat to our national security and choose to protect and recover species, and defend the living systems we all depend on,” the Oscar winner added. “Call your U.S. Representative today to urge them to vote ‘no’ on the ESA Amendments Act of 2025 (H.R. 1897). U.S. Capitol switchboard: 202-224-3121.”

DiCaprio posted while overseas filming “What Happens at Night,” his latest collaboration with director Martin Scorsese after the likes of “The Aviator,” “Gangs of New York,” “The Wolf of Wall Street,” “Shutter Island” and more. DiCaprio’s co-star is his fellow “Don’t Look Up” actor Jennifer Lawrence.

When he’s not being one of Hollywood’s A-list superstars, DiCaprio is also one of the town’s most outspoken environmentalists. During the 2024 presidential election, he threw his support behind Kamala Harris while bashing Donald Trump for ignoring climate change.

“Donald Trump continues to deny the facts. He continues to deny the science. He withdrew the United States from the Paris Climate Accords and rolled back critical environmental protections,” DiCaprio wrote in a statement at the time. “Now he’s promised the oil and gas industry that he’ll get rid of any regulation they want in exchange for a billion-dollar donation.”

He added, “Climate change is killing the earth and ruining our economy. We need a bold step forward to save our economy, our planet and ourselves. That’s why I’m voting for Kamala Harris.”

Check out DiCaprio’s latest post in the Instagram below.

The cryptocurrency markets have been energized again as Bitcoin ($BTC) surpassed the $78,000 mark, reaching its highest level in 11 weeks.

With investor risk appetite increasing, Scott Melker and macro strategist Noelle Acheson discussed the current state of the market and the dynamics behind Bitcoin’s rise on “The Wolf Of All Streets” channel.

Noelle Acheson stated that although Bitcoin is still viewed as a “risk asset” in the traditional financial world, its performance during times of crisis has shattered this perception.

Weekly chart showing the recent rise in $BTC price.

Experts, noting that Bitcoin has always gained value 60 days after seven major crises since 2020 (including the collapse of Silicon Valley Bank), argued that $BTC actually serves as a “protection against chaos.”

Related NewsNew Pro-Crypto Legislation on the Horizon in the U.S. – Here’s What the PACE Act Entails

One of the most critical points that stood out was the “worrying” signals from the bond market while stock markets were hitting record highs. The rise in 10-year Treasury yields to 4.2% – 4.3% indicates that markets have not yet found the relief they expected from the Fed’s interest rate cuts.

The broadcast stated that the hacking incidents in DeFi (Decentralized Finance) protocols last week and the vulnerabilities in platforms like “Kelp DAO” have created significant distrust in the market. This situation has driven institutional investors away from DeFi and towards Bitcoin, resulting in Bitcoin dominance reaching its highest level in the past year.

Analysts believe that data from derivative markets has not yet signaled “overheating” (frothy), leaving the door open for a new rally towards the $82,000-$84,000 levels. However, experts emphasize that investors should exercise caution due to speculation surrounding the Trump administration and global geopolitical risks.

Writer-director Jon Favreau successfully launched the Marvel Cinematic Universe with 2008’s Iron Man, but there was one MCU move he admits that he resisted behind the scenes: killing off Robert Downey Jr.’s beloved Tony Stark in 2019’s Avengers: Endgame.

Appearing on Jimmy Kimmel Live! on Tuesday to promote his upcoming Star Wars film The Mandalorian and Grogu, Favreau says he called up Anthony and Joe Russo to push back against their plan to end the character he helped create.

“I talked to the Russos, I said ‘I don’t know if people are gonna like … I don’t know, it’s really going to impact people because they were kids that grew up with that character,” Favreau said. “But I have to tell you, it was handled so well by them. And Gwyneth [Paltrow] and Robert did such a wonderful job acting, and I think it added a poignancy to it. I think they did a wonderful job. I was wrong.”

Favreau admitted even he got emotional when he watched the film. “I was choked up,” he said. “Even though it’s a movie, those people, those characters, have been part of my life for so long.”

Favreau added he’s “excited to see” Downey as Doctor Doom in the upcoming Avengers: Doomsday. He noted the “smartest thing I ever did” was give himself a cameo as the character Happy Hogan in the first Iron Man movie, because he’s been invited back to appear so many times in the franchise that the role has “put my kids through school.”

Asked who is “scarier,” Star Wars fans or MCU fans, Favreau diplomatically replied they’re “equally invested” in their respective franchises, but Star Wars fans have a longer attachment given the first film came out in 1977.

Favreau showed a new clip from TheMandalorian and Grogu, which you can watch around the 9-minute mark in the footage below. The film opens May 22.

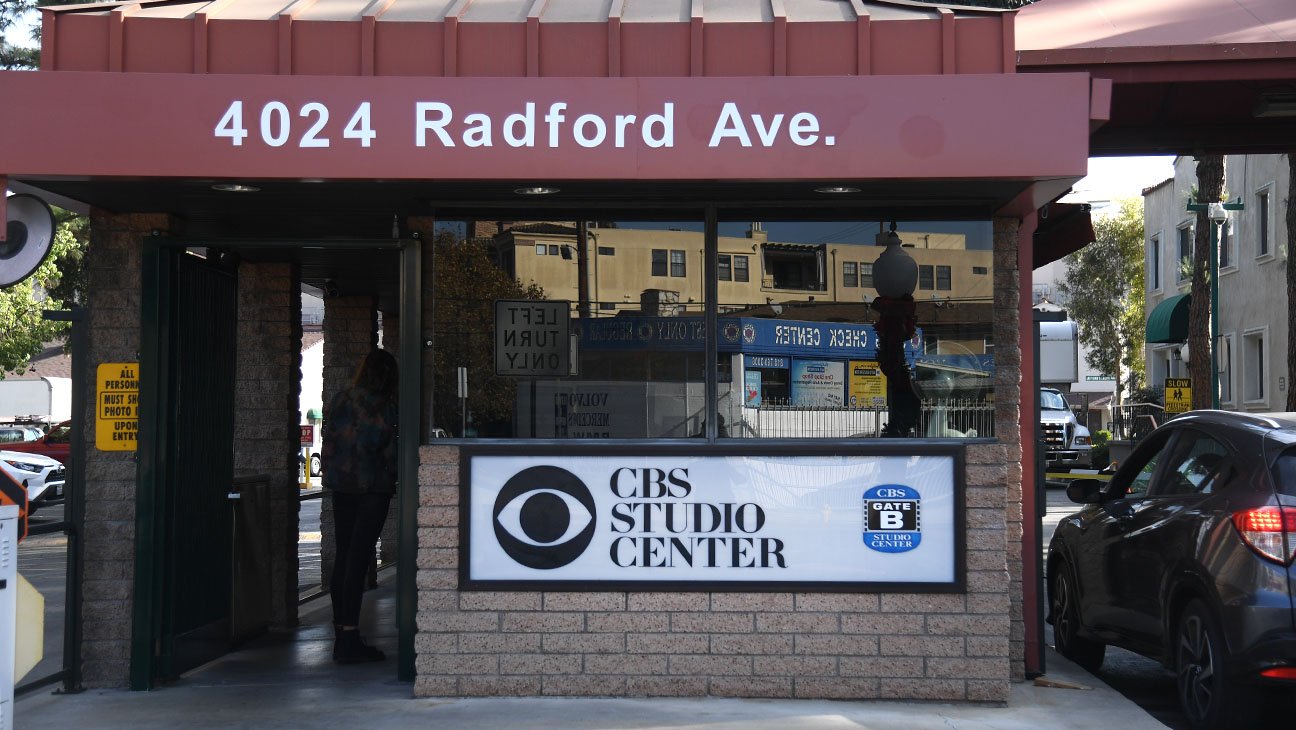

Netflix is nearing a deal to buy the historic Radford Studio Center lot, a purchase that would give the entertainment giant ownership of a major Los Angeles production campus.

Goldman Sachs, which took over the property earlier this year, is expected to sell the property for roughly $330 million, a source familiar with the deal tells The Hollywood Reporter, describing the agreement as “all but done.”

According to the source, Netflix didn’t participate in the first round of bids, which didn’t include other major studios and started roughly two months ago. Offers, most of which didn’t hit $300 million, were mostly submitted by entities looking for what could be a generational discount on the 55-acre property.

The sale is the first deal of its kind involving a major production campus in more than five years. It’s expected to set a baseline for lenders to rely on when renewing loans for comparable properties. “This is going to set the bar,” the source adds.

The buy could shake up Netflix’s base of operations in Los Angeles. For years, it has been the anchor tenant at Sunset Studios, making the ICON building its L.A. headquarters and occupying the EPIC and CUE buildings as part of the complex on Sunset Boulevard.

The streaming giant has a lease on those buildings through 2031 with the owner, Hudson Pacific Properties, which receives $27 million in base annualized rent from Netflix. As of early March, Hudson Pacific CEO Victor Coleman said at an investor conference that “our conversations with them are fluid” regarding future leases.

Netflix is the No. 2 tenant for Hudson Pacific among its office tenants, occupying 722,305 square feet of space, just behind Google, so a loss of the streaming giant would be a big one for the soundstage operator. (Amazon is its No. 3 tenant, and the company also has tech giants like Salesforce, PayPal and Elon Musk’s X AI leasing its properties.)

“We remain fully engaged with Netflix and believe this portfolio is the optimal long-term solution for their L.A. office needs, given the quality, location and expansion potential of these assets,” Coleman had said on the company’s February earnings call.

Netflix leases its Sunset Bronson Studios location (pictured during the 2023 labor strikes).

Tiffany Taylor/THR Staff

Radford, meanwhile, counts iconic titles like Seinfeld and Gilligan’s Island among the classic shows that have filmed on its soundstages. But even in corporate materials it describes itself as facing “decades of under-investment,” and renovation plans have been put in motion.

The historic studio was in the hands of the then-named ViacomCBS corp until 2021 when it was sold — as part of a slimming down of the Shari Redstone-run Paramount empire — to Hackman Capital Partners and Square Mile Capital Management for $1.85 billion.

The Michael Hackman-led firm had bet that studio infrastructure would be a hot commodity as majors had been bulking up on spending for streaming shows near the height of what was then a race to catch up to Netflix. Wall Street and private equity firms also saw the upside in studio lot infrastructure at the time, which was not too far removed from the COVID-19 pandemic, when office space was seen as a shakier bet.

Then, ahead of the 2023 dual labor strikes from the Writers Guild and SAG-AFTRA, the content spend pullback hit and stage occupancy started waning. (Now uncertainty about how AI workflows will impact content creation also factor in to big bets on soundstage infrastructure.)

Netflix could strike the deal as the value of L.A. studio real estate plunges amid a historic production slump in the region. Major soundstages recorded a 62 percent occupancy rate during the first six months of 2025, down one percent from anemic levels recorded in 2024, according to data released from local film office FilmLA in March. From 2016 to 2022, soundstages participating in the survey reported an average occupancy rate of at least 90 percent.

The filming downturn hit Radford, which has 22 soundstages, especially hard since fixed operating costs remain the same regardless of how many productions shoot on the property.

A green screen on set at the Radford lot in Studio City circa 2018.

Photographed By Yuri Hasegawa

Investment bank Goldman Sachs had taken over the Radford lot after Hackman defaulted on its mortgage, Bloomberg reported in January, citing a letter to investors that wasn’t made public. Hackman also operates the historic Raleigh Studios in Los Angeles, the Sony Pictures Animation Campus in Culver City and more major soundstages and production facilities.

Last year Hackman put a “For Sale” sign on a Raleigh sibling location, Saticoy Studios in Van Nuys, at an $18 million price tag, with an exec at the company telling THR that it was “non-core to our wider studio portfolio, which focuses on larger, flagship properties.” The main Raleigh Studios location, located on Melrose Avenue, has Netflix as the anchor tenant through 2031 as well.

That would mean that by 2031, Netflix may be able to be on the move at both Sunset and Raleigh studios should it choose to do so. And a Radford lot purchase — it boasts 22 soundstages, three backlot sets, 18 office buildings and 20 bungalows — could make for suitable new digs for Ted Sarandos and Co. in L.A. to go along with its restored Egyptian Theatre on Hollywood Blvd.

Netflix, which just received a $2.8 billion break up fee in connection with its abandoned pursuit of Warner Bros., has made an effort to build its soundstage bases over the years, outside of its L.A. office. Those include the formerly named ABQ Studios in Albuquerque, New Mexico as well as $1 billion to build its East coast base at the former site of Fort Monmouth, New Jersey (which won’t be ready for a few years).

That’s not counting the Los Gatos-based company’s expanding global office and studio space portfolio. This year alone, Netflix unveiled its Mexico City headquarters, opened a Buenos Aires, Argentina office and touted an expansion of its Poland central European hub as it builds infrastructure to provide a content pipeline to serve its 325 million subscribers.

Sunset Studios soundstage operator Hudson Pacific, meanwhile, has looked to the East coast for an expansion, opening its purpose-built Sunset Pier 94 Studios in Manhattan in January with Paramount Television Studios’ Dexter: Resurrection signing on to produce its second season at the location.

April 22 Story updated throughout with additional reporting.

In the lawsuit Sun alleged that World Liberty illegally froze his holdings of tokens issued by the company.

Published On 22 Apr 202622 Apr 2026

Crypto entrepreneur Justin Sun has sued World Liberty Financial, the digital currency venture cofounded by United States President Donald Trump and his sons, alleging that World Liberty illegally froze his holdings of tokens issued by the company.

Sun alleged in the lawsuit, filed in a federal court in California on Tuesday, that World Liberty secretly installed tools to prevent the sale of his tokens after they became tradable in September 2025. The lawsuit also alleges that World Liberty threatened to “burn” – or permanently delete – his holdings, even while they were in Sun’s digital wallet.

Recommended Stories

list of 4 itemsend of list

Sun, the Hong Kong-based founder of the Tron cryptocurrency, bought $45m of WLFI tokens – some 3 billion – and was later awarded a further 1 billion tokens after being named as an adviser to World Liberty, the lawsuit said.

Sun’s portfolio of 4 billion WLFI tokens is worth roughly $320m, according to a Reuters news agency calculation based on the latest WLFI price.

World Liberty Financial declined to comment on the lawsuit. A spokesperson for the company had told Reuters earlier this week that Sun “is not an advisor at World Liberty Financial, and he has never held an operational role in the company”.

The White House did not immediately respond to a request for comment.

World Liberty is the most prominent of several lucrative crypto businesses cofounded or controlled by the Trump family, which has already made more than $1bn from World Liberty, according to a Reuters analysis. World Liberty’s bylaws state that 75 percent of the revenue from WLFI token sales is routed to the Trumps.

World Liberty is under increasing scrutiny from some of its investors, who have complained for months about what they describe as the company’s lack of transparency, centralised governance structure and failure to respond to community complaints.

In the lawsuit, Sun described himself as “one of World Liberty’s anchor investors”.

World Liberty’s structure means that the WLFI tokens Sun bought in 2024 are not equivalent to standard company shares. The tokens do not carry ownership in the company, and holders are not entitled to dividends, although they do gain a limited say in the company’s governance.

Souring relationship

The lawsuit caps a dramatic deterioration of relations between Sun and World Liberty.

In September, Sun claimed that the company had frozen his token holdings, and earlier this month, he alleged in a post on social media platform X that World Liberty had secretly embedded what he described as a “backdoor blacklisting function” in the blockchain-based contracts used for the tokens.

That gave World Liberty “unilateral power” to “freeze, restrict, and effectively confiscate the property rights” of token holders without cause or recourse, Sun wrote on X.

World Liberty at that time responded to Sun’s allegations with a post on X that said: “We have the contracts. We have the evidence. We have the truth. See you in court pal.”

The lawsuit said Sun “has long been [and remains] an ardent supporter of President Trump and the Trump family”.

Frozen out

The lawsuit alleges that World Liberty representatives “repeatedly contacted and pressured” Sun to invest additional capital in the venture between April and July 2025, including requests to commit to acquiring $200m in a separate World Liberty stablecoin token and to acquire an equity stake in the company.

Sun said in a post on X on Wednesday that he had “tried in good faith” to resolve his complaints with World Liberty, adding that its team “refused my requests to unfreeze my tokens and restore my rights as a token holder”.

A measure proposed by the company last week would restrict early investors holding a combined 17 billion tokens from being able to trade all of their tokens until 2030, a year after the president is scheduled to leave office.

Sun said he “strongly opposes” the new governance proposal, but could not vote on it as World Liberty had frozen his early investor tokens.

Sun has also invested heavily in Trump’s so-called meme coin.

Trump has launched a slate of crypto-friendly policies since returning to the White House in January 2025.

In March, the Securities and Exchange Commission settled a 2023 lawsuit against Sun for $10m. The lawsuit had alleged fraud, selling unregistered crypto securities and hiding payments to celebrities to promote his products. Sun made no admission of wrongdoing.