The rumor followed a familiar wartime script. Iran’s Islamic Revolutionary Guard Corps claimed it had struck Benjamin Netanyahu’s office. Then came the forged screenshots — fake posts from the Israeli prime minister’s official account announcing he was dead. Then came the AI furore over a low-resolution freeze-frame from a press conference that, at the right angle, appeared to show Netanyahu’s right hand sporting six fingers, leading contrarian commentators to take victory laps.

Conservative influencer Candace Owens amplified the claims loudly on X, demanding to know where Netanyahu was and why his office was “releasing and deleting fake AI videos.” Iran’s Tasnim News Agency — run by the Islamic Revolutionary Guard Corps — published an article titled “New Video of Netanyahu Proves Fake,” cataloguing alleged clear signs that a subsequent coffee shop clip, posted by Netanyahu’s own account to debunk the rumors, was itself generated by artificial intelligence. The conspiracy had become self-sealing; every refutation was recast as fresh evidence.

But while the fact-checkers scrambled and the podcasters speculated, one data source offered a clean, immediate signal. On Polymarket, the world’s largest crypto prediction market, the contract for “Netanyahu out by March 31” was trading at around 4 to 5 cents, implying a roughly 4 to 5% probability of him leaving office before the end of the month. The market didn’t move. For anyone paying attention to that number, the entire conspiracy theory collapsed in a single glance.

Polymarket volume (Dune Analytics)

A record-breaking backdrop

To understand why the Netanyahu conspiracy took hold when it did, you need to understand the information environment it emerged from.

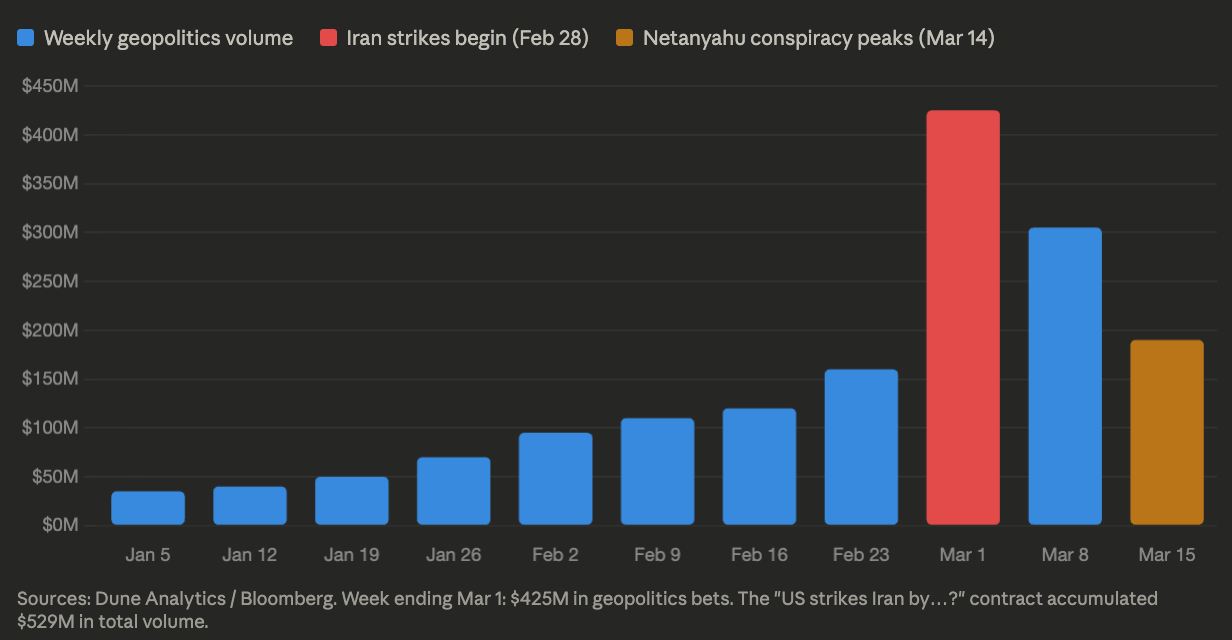

Since the U.S. and Israel launched strikes on Iran on Feb. 28, Polymarket has been transformed into something closer to a real-time geopolitical intelligence terminal. In the week ending March 1, bettors placed $425 million in geopolitics wagers on the platform alone — up from $163 million the prior week — with total platform wagering hitting a record $2.4 billion. The “US strikes Iran by…?” contract accumulated $529 million in total volume, making it one of the largest single markets Polymarket has ever hosted and the fourth-largest in its entire “Politics” category.

It is a remarkable trajectory for a platform that processed $73 million in total trading volume in 2023 and was pushed offshore by a CFTC settlement a year later. By 2025, Polymarket had processed approximately $22 billion in notional trading volume across the year — a figure that underscores how quickly the platform has moved from crypto curiosity to mainstream financial infrastructure.

This is no longer a crypto curiosity. In October 2025, the Intercontinental Exchange, parent company of the New York Stock Exchange, invested $2 billion into Polymarket at a $9 billion valuation, and launched a “Polymarket Signals and Sentiment” tool that feeds real-time prediction market data directly to Wall Street trading desks. When the Iran war began, equity and oil futures markets were closed for the weekend. Polymarket was not.

The market as instant truth machine

Prediction markets don’t have death contracts in the conventional sense. What Polymarket offers instead are “politician out by X date” markets, which resolve “Yes” if a leader resigns, is removed, or steps down. They don’t directly price the probability of death. But in a context where the conspiracy theory is that Netanyahu has been killed and the government is conducting a cover-up, these contracts function as a powerful proxy.

The logic is simple. A leader who has died or been incapacitated cannot indefinitely run a country from office. Eventually, a resignation, a removal or a credible leak would surface. And if any of that happened, the payout on a “Yes” share at 5 cents would be enormous: a $1 payout on a 5-cent share is a 20-to-1 return.

One trader was willing to make that bet at scale. A single Polymarket account placed $151,000 on Netanyahu being out before March 31, accumulating nearly 3.8 million shares at 4.7 cents each. If correct, the position would pay out $3.8 million. It is currently underwater by roughly $26,000.

That number is the ceiling of rational conviction in the conspiracy. At the height of the online hysteria, the most aggressive speculator on record was willing to stake $150,000 on the theory — implying he knew the odds were long. The market as a whole put the probability at around 5%. Social media said it was certain. The money said otherwise.

“Whether a politician is in or out of office is a very economically meaningful outcome for a lot of people,” said Aaron Brogan, a managing attorney at Brogan Law who has advised on prediction market regulation. “These are exactly the kinds of markets that event contract rules were designed to accommodate.”

Why the odds are hard to fake

The 2024 US election cycle offered a masterclass in prediction market efficiency — and the limits of efforts to dismiss its signals. When Polymarket showed Donald Trump trading at a substantial premium over Kamala Harris, critics cried manipulation. A French trader, they alleged, had artificially pumped Trump’s odds using multiple accounts for political purposes.

The experts weren’t buying it. As Flip Pidot, co-founder of American Civics Exchange, told CoinDesk at the time: a true manipulator trying to move the price would simply pile in blindly and let themselves get filled at worsening prices. The French trader did the opposite — splitting orders strategically across accounts to minimize slippage. That is what profit-seeking looks like, not propaganda.

The deeper reason manipulation struggles to stick is expected value arbitrage. If a price is artificially depressed or inflated, profit-hungry traders pile in to exploit the gap until it closes. Cross-market arbitrage reinforces this: Polymarket prices in real time against Kalshi, Betfair, and others. If odds drift meaningfully out of line across platforms, traders immediately sell the higher price and buy the lower one, synchronizing markets toward a consensus.

Harry Crane, a statistics professor at Rutgers University who studies prediction markets, sees the Netanyahu episode as a near-perfect illustration of this dynamic. “These markets are an antidote to propaganda precisely because their resolution rules anchor outcomes to verifiable sources rather than narrative,” he told CoinDesk. “I understand why governments want to limit them — not because of concerns over leaking classified information, but because verifiable price signals are harder to control.”

That framing maps directly onto the Netanyahu conspiracy. The people claiming he was dead were doing structurally the same thing as those who cried Polymarket was rigged in 2024: attacking the signal rather than engaging with it.

What the market is actually pricing — and what it isn’t

Crane is careful about the limits of the signal, and his caveat is worth sitting with.

“The market is only pricing the probability that Netanyahu is verifiably out of office under these rules,” he said. The resolution criteria state that the contract resolves “Yes” if Netanyahu announces his resignation or is otherwise removed from office, confirmed by official sources or a consensus of credible reporting. If a government concealed a leader’s death so completely that no credible source ever confirmed it, the market could resolve “No” — faithfully, correctly under its own rules, and yet without capturing the underlying reality.

That dynamic was playing out in real time. Domer — a well-known prediction market trader who goes by ImJustKen online — was publicly holding a No position on Netanyahu leaving office before March 31. Not because he was certain Netanyahu was alive, but because he didn’t believe a departure would ever be confirmed under the market’s resolution criteria, even if it occurred. He was pricing the verification gap, not the conspiracy itself.

But that caveat reveals something important about the conspiracy itself. The Netanyahu death rumor only holds together if you believe in a cover-up so total — encompassing Israeli officials, international media, independent fact-checkers, and Netanyahu’s own social media accounts simultaneously — that no verifiable evidence would ever surface. At that point, the conspiracy has become unfalsifiable by design. An unfalsifiable claim is one no rational actor should stake capital on.

This is the key distinction from traditional fact-checking. A fact-checker requires institutional credibility, research time, and editorial process — all of which conspiracy theories are engineered to preemptively undermine. A Polymarket price requires none of that. It requires only that someone, somewhere, believes the opposite enough to put real money on it. When no one does, that is its own kind of proof.

The contrast case: Khamenei

The clearest evidence that these markets work as a truth signal — and not merely as a null result — is what happened with the Khamenei contract.

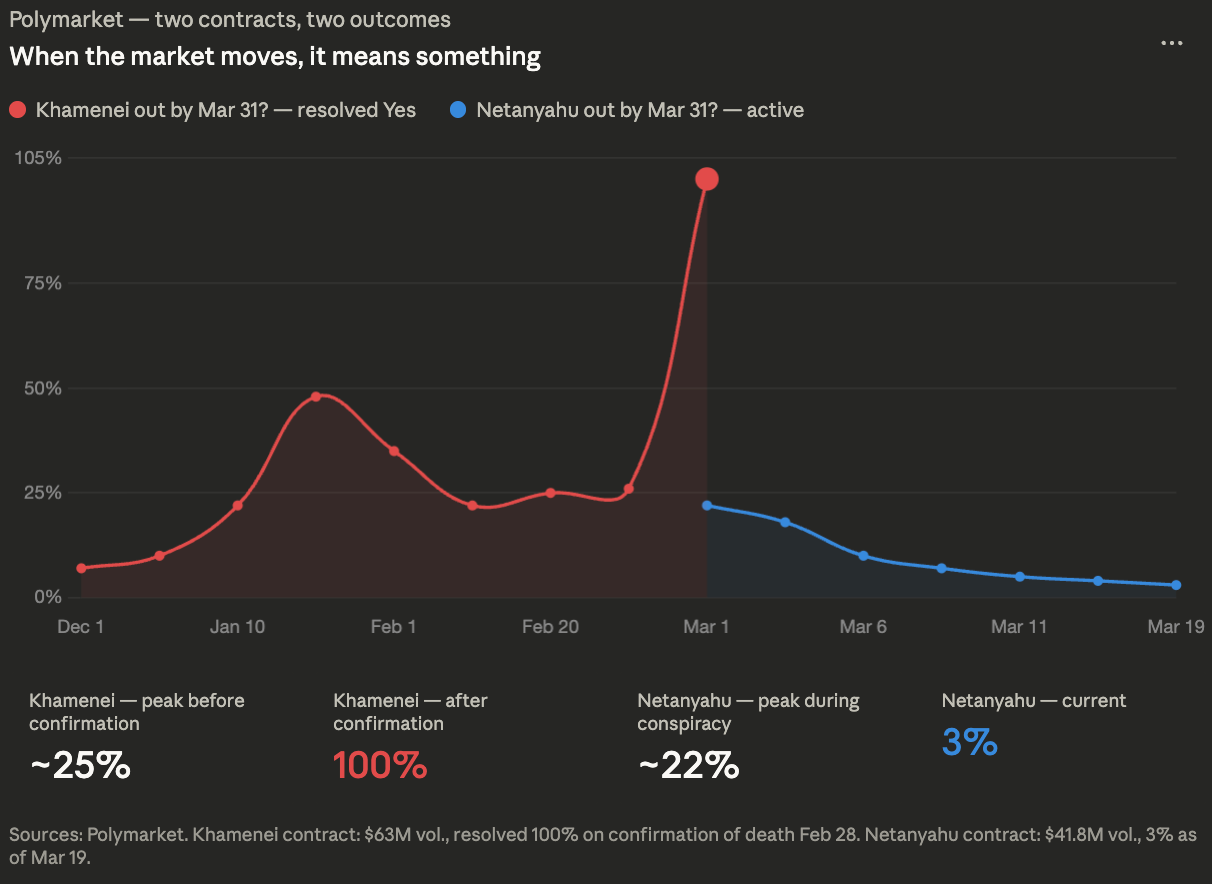

When Iranian Supreme Leader Ali Khamenei was killed in the February 28 strikes, the “Khamenei out as Supreme Leader by March 31” contract on Polymarket behaved exactly as you would expect from an efficient market. It had hovered between 25% and 50% through January and February as tensions built, pricing genuine uncertainty about an escalating conflict. Then, when Iranian state TV confirmed his death, it spiked vertically to 100%. The contract drew $45 million in volume. The top trader made $757,000 on a yes bet. Four others cleared six figures.

The Netanyahu market did not do this. It stubbornly remained below 5 cents throughout the conspiracy cycle. The crowd that correctly priced Khamenei’s death — and got paid for it — looked at the Netanyahu claims and declined to move.

Price movements on Polymarket (Polymarket)

The regulatory storm gathering overhead

The informational value of these markets is being stress-tested at exactly the moment when political pressure against them is reaching its peak.

When Khamenei was killed, Kalshi — Polymarket’s CFTC-regulated rival — invoked a “death carveout” buried in its contract terms, settling its Khamenei positions at the last traded price before his death: roughly 39.5 cents rather than the full dollar. Polymarket, which carries no such carveout, paid out in full. A $54 million class action lawsuit against Kalshi followed.

The inconsistency in Kalshi’s approach has been pointed out sharply. In late 2024, Kalshi had run a market on whether a 100-year-old Jimmy Carter would attend Trump’s inauguration. When Carter died before it took place, Kalshi settled that contract to “No” — resolving a market directly via death, without invoking any carveout. As Crane has noted, the application of its death carveout appears to have been selective: they settle on death, just not when it’s expensive.

Kalshi disputes the characterization. “Our rules were clear from the beginning, we never changed them, and we settled based on the rules,” a spokesperson said. The company added that it reimbursed all fees and net losses out of pocket following the Khamenei settlement — “to the tune of millions of dollars” — ensuring no user lost money on the market. “Kalshi is a peer-to-peer exchange and does not profit from user losses. We have no incentive not to pay out our users, but we need to follow the rules of the exchange and the rule of law.”

On the legislative push, the company struck a conciliatory tone. “Kalshi already bans insider trading and markets directly tied to death and war,” a spokesperson said. “As a US-based exchange, we support regulators and policymakers from both sides of the aisle in their efforts to keep these markets safe and responsible in America.”

Kalshi declined to comment on record about the consistency of the death carveout as applied to the Khamenei contract versus the Carter market, or on the current status of the class action lawsuit.

Six Democratic senators, led by Adam Schiff, have written to the CFTC demanding a categorical ban on contracts that “resolve upon or closely correlate to an individual’s death.” Separately, senators Merkley and Klobuchar have introduced the End Prediction Market Corruption Act, which would bar the president, vice president, members of Congress, and their immediate families from trading event contracts, and impose fines and profit clawbacks for violations — citing the well-timed wagers on US strikes and Iranian leadership changes that netted some traders hundreds of thousands of dollars.

Blockchain analytics firm Bubblemaps identified six newly created wallets that collectively netted $1.2 million betting on the timing of US strikes on Iran, with accounts funded within 24 hours of the attack. One trader turned roughly $60,000 into nearly $500,000.

Brogan is skeptical that the legislative push has the momentum to land. “This is largely Democratic senators using the legislative process to generate political capital,” he said. “The conditions under which that legislation actually passes are where something really calamitous happens — some kind of market collapse or scandal that forces politicians to make an example of the industry. Without that, I don’t think there’s sufficient political capital to move it.”

He also draws a clear distinction between Polymarket’s legal exposure and Kalshi’s. “The restrictions Kalshi faces are not directly applicable to Polymarket,” Brogan said. Polymarket is not a CFTC-regulated US exchange — a status that stems from a 2021 settlement that pushed it offshore and barred US users from accessing it directly. That remains its largest single legal exposure, Brogan noted, though he pointed out that the Trump administration has shown little appetite for pursuing the kind of action the Biden administration explored against Polymarket CEO Shayne Coplan in early 2025.

Crane, for his part, is unambiguous about what would be lost if the legislative push succeeded. “These markets have genuine informational value and can counter propaganda,” he said. “That’s the case study here — a market involving war and the fate of a political leader doing exactly what its critics say it shouldn’t exist to do.”

There is also a state-level front opening up. Arizona recently charged Kalshi with operating an illegal gambling operation — part of a broader conflict between states that regulate and tax traditional gambling markets and federally-overseen prediction markets that sit outside their control. “The question that ultimately matters is whether federal law will preempt state law on this,” Brogan said. “There are courts hearing that question right now.”

What the crowd gets right — and what it can’t fix

None of this is to say prediction markets are infallible. Crane notes that nearly 25% of Polymarket’s historical volume has been attributed to wash trading — artificial activity generated by users trying to position themselves for a potential token airdrop — a figure that Columbia University researchers found peaked at around 60% in December 2024 before falling sharply. Wash trading inflates headline volume without necessarily biasing prices, but it is a legitimate caveat to the “wisdom of crowds” narrative.

The more fundamental limitation is what Crane identified in his answer to the manipulation question: a sufficiently coordinated disinformation campaign could, in theory, move a market — especially a smaller one. The Netanyahu “out by March 31” contract had enough liquidity to make that expensive, but not impossible.

What prediction markets cannot do is replace the underlying information infrastructure they depend on. They resolve against credible sources. If those sources are corrupted or silent — as Iranian state media clearly was throughout this episode — the market’s signal is only as good as the resolution criteria it is anchored to.

But in the Netanyahu case, that is precisely where the conspiracy fell apart. The rumor required a cover-up so comprehensive that no Israeli official, no international journalist, no independent fact-checker, and no market trader with real money on the line would ever find confirmation. The market priced that scenario at 5 cents. It was right.

When Candace Owens was demanding to know where Bibi was, Polymarket already had an answer. It just costs a few pennies to read it.