Treasury Secretary Scott Bessent said the department is moving at a “deliberate speed” to establish a strategic bitcoin reserve while continuing to push for passage of a major cryptocurrency market structure bill this summer.

Speaking on Wednesday during a Senate Finance Committee hearing to discuss the 2027 budget, Bessent pressed lawmakers to “get behind” the bill, called the Clarity Act, and said he wants that legislation passed this summer.

“It’s very necessary to bring U.S. best practices onshore, and we work tirelessly in terms of custodying these assets and making the U.S. the innovation capital of the world,” Bessent said.

Lawmakers have spent the past year working to pass the Clarity Act, which would regulate the digital asset industry for the first time at the federal level. A version of the bill passed out of the full House last year, but has since found itself stuck in the Senate following hurdles around the treatment of stablecoin rewards, software developer protections and how to address conflicts of interest following President Donald Trump’s crypto ventures.

Time is dwindling now to pass the Clarity Act as priorities on Capitol Hill turn to budget bills before the end of the year, and midterm elections in November are expected to take up lawmakers’ time after the summer.

As debate over the bill continues, Bessent told lawmakers on Wednesday that his Treasury Department is moving forward with a strategic bitcoin reserve. In the first few months of the new presidential administration, President Trump signed an executive order to create that strategic bitcoin reserve, funded mainly through bitcoin already owned by the government through criminal or civil forfeitures, and a separate digital asset stockpile.

In April, the executive director of the President’s Council of Advisors for Digital Assets, Patrick Witt, said there would be a “big announcement” coming in the next few weeks on the next steps for the reserve.

On Wednesday, Bessent called the process complicated, but said they are moving forward.

“We are proceeding with all deliberate speed, and we are making sure that as we are doing this in this complicated process, we use best practices and things will be durable for the future,” Bessent said.

Global payments giant Mastercard is expanding its global settlement infrastructure to support additional intraday, weekend, and holiday settlement windows, as well as on-chain settlement using regulated stablecoins, the company announced Wednesday.

The company said the upgrades will provide issuers and acquirers with more options for managing liquidity and settling card transactions beyond traditional banking hours. The enhancements are intended to work alongside existing settlement processes and support use cases such as cross-border payments, treasury management, and business payouts.

Stablecoin settlement will be available through a range of regulated digital assets, including Circle’s USDC, Paxos-issued $PYUSD, $USDG, USDP, Ripple’s $RLUSD, and SoFiUSD. Mastercard plans to support these assets across several blockchain networks, including Ethereum, Solana, Polygon, Base, Arbitrum, XRPL, Canton, and Tempo.

“As demand grows for faster and more flexible movement of money, organizations are increasingly seeking infrastructure that can operate beyond traditional banking hours,” Kash Razzaghi, Circle’s chief commercial officer, said in a statement. “Mastercard’s expanded settlement capabilities help meet that need, offering greater choice in how value is transferred and settled.”

Initial ecosystem participants are expected to include ARQ, CBW Bank, Cross River, Lead Bank, and Nuvei, with deployments beginning in the US and Latin America before expanding to additional regions.

“We’ve seen firsthand the accelerating demand from our partners for faster, more transparent settlement, and stablecoins have emerged as a powerful tool to meet that need,” Luca Cosentino, head of on-chain finance at Cross River, commented on the move. ”Mastercard’s decision to bring on-chain settlement to its global network validates what we’ve been building toward: a future where digital asset rails operate seamlessly alongside traditional payments infrastructure.”

Mastercard said the initiative represents the next phase of its digital asset strategy, allowing financial institutions to access both traditional and blockchain-based settlement through the same network infrastructure while preserving established safeguards and operational standards.

“Mastercard’s move into on-chain settlement is a landmark validation that blockchain technology is ready for the world’s most critical payment infrastructure,” Jack McDonald, senior vice president of stablecoins at Ripple, said. “$RLUSD’s inclusion in Mastercard’s global settlement network reflects growing demand for trusted, regulated stablecoins built for real-world financial use cases on public blockchains like the $XRP Ledger. We’re excited to support the next evolution of faster, more flexible, always-on settlement.”

Mastercard’s US money transfer subsidiary, MTS US, has been granted a NYDFS BitLicense, allowing it to support settlement using stablecoins and tokenized deposits. Mastercard said the approval underscored its focus on regulatory standards and trusted digital payment infrastructure.

With the planned acquisition of BVNK and partnerships with Circle and Paxos, Mastercard is building a comprehensive infrastructure for stablecoin-based payments and settlement.

“The future of settlement is programmable, instant and global,” Peter Jonas, chief revenue officer of Paxos, stated. “Paxos’s regulated infrastructure gives partners like Mastercard a trusted path to on-chain settlement using $PYUSD, $USDG, and USDP that works seamlessly alongside existing systems, helping advance more efficient payment flows.”

Coinbase Ventures invested in Ethena through an open market purchase of $ENA as Coinbase expanded its partnership with the onchain synthetic dollar protocol.

Ethena and @coinbase have partnered to grow onchain finance and savings products for their 100m+ userbase, with the first growth initiative launching next week.

Alongside this partnership Coinbase Ventures have also made their first investment into Ethena on the open market. https://t.co/RGPUSlTRdU pic.twitter.com/6tBW404lYv

— Ethena (@ethena) June 2, 2026

The partnership makes Coinbase Ethena’s primary custodian, wallet provider, and perpetuals venue, supporting security and operations across more than $5 billion in assets. Ethena said $USDe is also coming to Base and the broader Coinbase ecosystem as the companies move to expand onchain finance and savings products.

Coinbase Ventures said Ethena is a critical player in onchain finance and that it is backing the protocol through its first open market investment in $ENA.

The move deepens Coinbase’s relationship with Ethena after Coinbase Prime was selected by Ethena in 2024 to provide custody, USDC, and self custodial wallet services for the protocol.

Ethena founder Guy Young said the upcoming integration will mark the first time Ethena products become available to Coinbase’s user base of more than 100 million. He said the evolving Clarity Act could create further tailwinds for onchain native products such as $USDe, particularly around idle balances on exchanges.

$ENA, the native token of Ethena, rose more than 15% on the news and was trading near $0.96 at press time, according to CoinGecko data.

Coinbase shares were trading near $173, down about 4% on the day, after opening at $176.85 and touching an intraday low of $171.70, according to Yahoo Finance data.

Payward, the parent company of crypto exchange Kraken, will soon allow retail investors outside traditional brokerage channels to participate in US listed initial public offerings through tokenized equity allocations at the IPO price.

The company said its xStocks framework will let eligible customers of Kraken and select xStocks Alliance members submit interest in upcoming US listed IPOs before a company goes public. If allocations are approved, users would receive tokenized shares at the offering price on listing day through the exchange they already use.

The product targets a part of capital markets that has historically favored institutional investors, private banking clients, and platforms with direct underwriter relationships. Retail investors often gain access only after shares begin trading publicly, when prices may already have moved above the IPO level.

Under the process, partner exchanges will open an indication of interest window in the weeks before a listing. Customers can submit non binding offers within the company’s indicated price range, while Payward Services aggregates demand and works with an underwriting syndicate on behalf of xStocks Alliance partners.

On listing day, finalized IPO allocations will be tokenized and distributed to eligible customers. Each tokenized equity will be backed 1:1 by the underlying share, which will be held in custody by a regulated entity.

Mark Greenberg, Global Head of Payward Services, said going public should mean public to everyone. He added that access to IPO pricing has long depended on geography and net worth, while Payward’s xStocks infrastructure aims to make similar access available to retail investors in markets such as Medellín, Madrid, and Malaysia.

The offering builds on xStocks, Payward Services’ tokenized equities framework designed to make equity exposure portable across crypto platforms. The company said xStocks tokens are blockchain agnostic, interoperable across chains, composable with DeFi protocols, and available through platforms in the xStocks Alliance.

Payward said the xStocks framework has processed more than $30 billion in total transaction volume in its first year, including more than $6 billion settled onchain across over 125,000 unique holders globally.

Payward said the first tokenized IPOs powered by xStocks will be available in the coming weeks to customers of Kraken and other xStocks Alliance members, with plans to expand the offering to additional markets and partners.

Revolut expects to start operating its US bank next year as the UK fintech expands its push into regulated banking, stablecoins, and multi asset financial services, according to a Reuters report.

The company’s US bank is expected to offer FDIC insured products, including high yield investment and checking accounts, according to Cetin Duransoy, Revolut’s recently appointed US CEO. US clients will also have access to stablecoins, deposits in multiple currencies, stock trading, and crypto trading.

Revolut applied for a US national bank charter in March. Duransoy said the bank is expected to be headquartered in Stamford, Connecticut, with an additional office in New York.

The company plans to focus first on clients with international financial needs. Revolut’s app supports services in more than 30 currencies, positioning the bank to serve retail and business customers that need access to dollars, rupees, Latin American currencies, and other foreign exchange products.

Revolut will not operate physical branches, though clients will have access to ATM networks.

The expansion comes as Revolut scales its US ambitions from a relatively small base. The company has 75 million clients globally, including 1 million in the US. Many of its US users already know the fintech through its operations in Europe, Latin America, or Asia.

Revolut reported 4.5 billion pounds, or about $6 billion, in revenue last year, along with 1.3 billion pounds, or roughly $1.75 billion, in net profit. The privately held company was valued at $75 billion in its latest funding round.

CEO Nik Storonsky has said Revolut does not plan to list its shares before 2028.

Welcome to our institutional newsletter, Crypto Long & Short. This week:

Alex Tapscott on the stalling of the CLARITY Act and how it’s impacting the average American consumer.

Aisha Hunt writes that crypto will grow by upgrading Wall Street’s trusted products rather than replacing them.

Top headlines institutions should pay attention to by Helene Braun

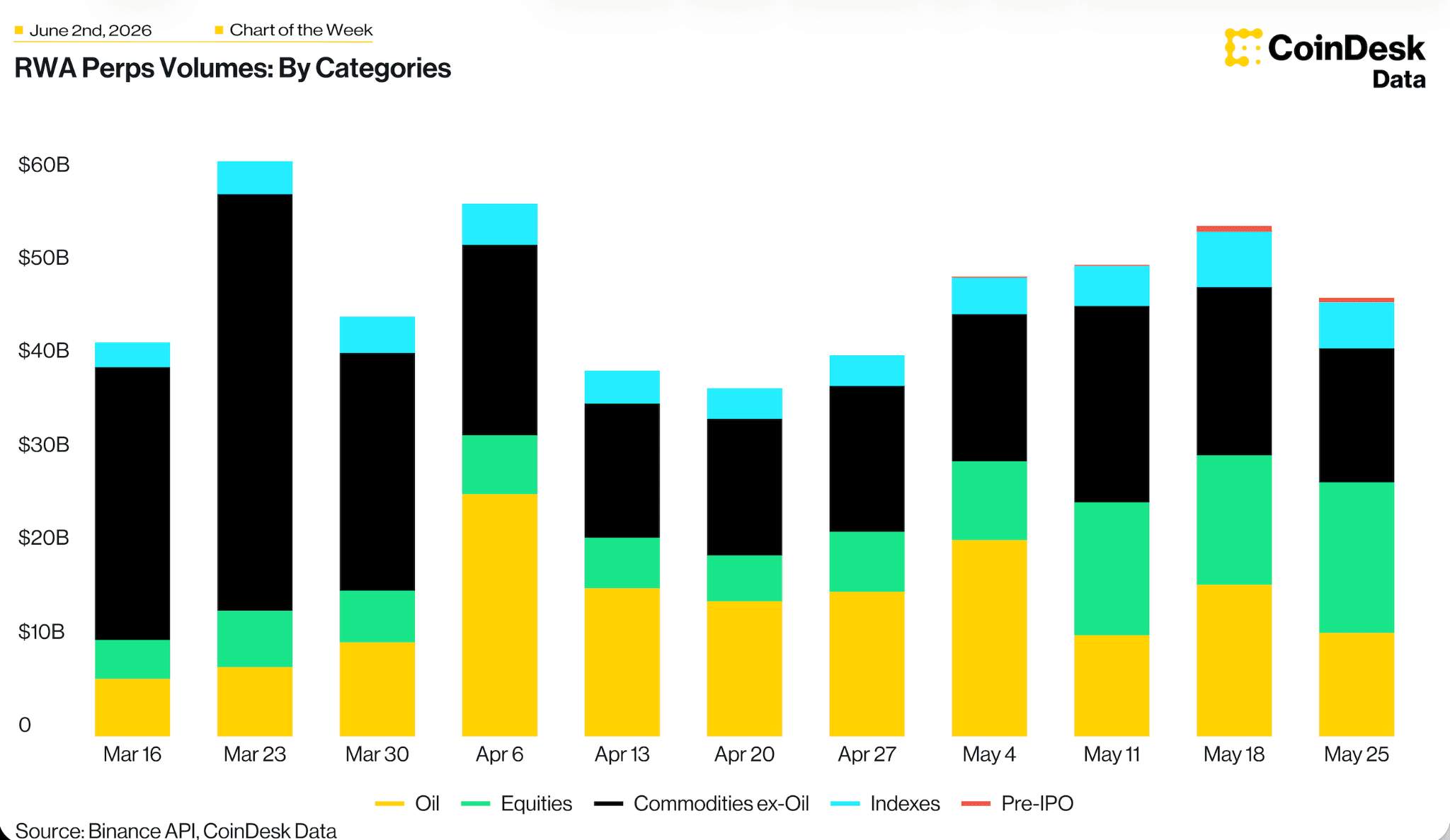

“RWA Perp Volume by Category: Equities Overtake Commodities” in Chart of the Week

-Alexandra Levis

Expert Insights

What about the American consumer?

By Alex Tapscott, CEO, CMCC Global Capital Markets

The little guy is getting lost in the political horse-trading around the CLARITY Act.

The U.S. Senate Banking Committee recently advanced the Digital Asset Market CLARITY Act, legislation that, if enacted, could finally establish clear rules for digital assets in the United States. The bill has survived months of bipartisan negotiations and horse trading between banking interests and upstart fintech companies.

A bipartisan compromise brokered by Senators Thom Tillis (R-NC) and Angela Alsobrooks (D-MD) broke a log-jam that had slowed down the bill’s progress. In the end, the banks got most of what they wanted in this “deal”: the legislation explicitly prevents fintech platforms from treating stablecoins, digital assets backed by dollars, as interest bearing accounts, while still permitting them to pay rewards and bonuses, as banks and credit card issuers do.

That should have ended the debate. Yet banking lobby groups are demanding tighter restrictions to eliminate many forms of consumer rewards altogether. Clearly, they seek to squash this already compromised bill before a full Senate vote, so that it never reaches the Resolute Desk.

Lost amid the political wrangling of crypto and banking interests is the average American consumer.

According to the Consumer Financial Protection Bureau (CFPB), Americans paid roughly $5.8 billion in overdraft fees in 2023, even after years of industry efforts to reduce so-called “junk fees.” Overdraft charges disproportionately hit financially vulnerable households, with nearly 80% of fees concentrated among 9% of accounts. And then there are account minimums, wire charges and payment delays, which add friction. Meanwhile, the average savings rate is only 0.38%.

Consumers want financial services to move faster, cost less and earn them more.

Stablecoins are gaining popularity because they herald a world where digital dollars move across the internet as cheaply and seamlessly as a WhatsApp message. They can lower remittance costs, improve access to digital commerce, expedite real-time payments and create new ways for consumers to save, spend and transact online.

And Americans are asking for CLARITY because many already use these tools. According to the Crypto Council for Innovation, one in five American adults now owns cryptocurrency. That’s roughly 68.5 million people. Stablecoins are among the fastest-growing categories of digital assets, particularly among younger consumers, immigrants, freelancers and underserved communities seeking faster and cheaper financial tools. Four in five merchants believe accepting crypto could help attract new customers, while 73% of small business owners expect crypto payments to grow.

That’s what makes this debate so politically mystifying. For years, progressives argued that concentrated financial power harmed consumers and Main Street. They criticized large banks for extracting rents while lobbying against regulations that diluted bank influence. Those critiques were often correct. Today some of those progressives, like Elizabeth Warren, who championed the Consumer Financial Protection Bureau, are now defending banking profits against a technology that could inject real competition into financial services and empower consumers and small businesses.

Congress should pass CLARITY in its current form to benefit American consumers and preserve American competitiveness and leadership in the next era of financial technology. This lead is by no means assured: today, 88% of global crypto trading volume occurs on non-U.S.-based exchanges, while foreign-issued stablecoins account for 75% of stablecoin volume. Over the past decade, the U.S. share of global crypto developers has fallen from 38% to just 19%.

Do American politicians want their country to continue leading, or do they prefer watching such financial transformation from the sidelines?

In the 1990s, the Clinton administration helped usher in the commercial internet through the Telecommunications Act of 1996, a bipartisan effort expanding innovation and competition. Now, Congress has an opportunity to unleash the new internet of value by passing CLARITY.

Under GENIUS and CLARITY, stablecoin issuers must meet strong reserve requirements, transparency obligations, anti-money laundering standards, cybersecurity rules and consumer protections. Sensible public policy will unleash investment and innovation, as it did in the internet era.

This story need not end in conflict between banks and blockchains. Incumbents can just as easily embrace blockchain and its various benefits, from real-time global settlement and tokenized assets, to new forms of on-chain lending, payments, savings and commerce.

The question is whether lawmakers will vote to lead this next technological revolution and advance the interests of American consumers or cede the future to entrenched interests.

Principled Perspectives

Why Crypto May Need ETFs More Than ETFs Need Crypto

By Aisha Hunt, founder of Kelley Hunt, PLLC

Crypto spent its first decade trying to replace Wall Street. Its next trillion dollars may come from partnering with it. The first wave of tokenization focused on creating new assets, new venues and new systems outside traditional finance. Some of that innovation mattered. Much of it struggled with the same problem: markets do not scale on technology alone. They scale on trust, liquidity and distribution. That reality favors ETFs.

The ETF wrapper became one of the most successful financial products of the modern era because it solved practical investor problems at scale: low-cost access, transparency, intraday liquidity, operational simplicity and broad distribution across brokerage platforms and advisory channels.

Those advantages took decades to build. Tokenization does not erase them. In fact, it may amplify them. If blockchain rails can be integrated into ETFs, investors may not have to choose between innovation and protection. They could gain exposure to familiar products with the potential benefits of faster settlement, programmable ownership, collateral mobility and broader digital interoperability, all inside a structure already trusted by institutions, advisors and retail investors.

That is a far bigger commercial opportunity than asking trillions of dollars to migrate into unfamiliar vehicles. This is why one underappreciated development matters. On January 21, 2026, F/m Investments LLC and The RBB Fund, Inc. filed what is believed to be the first exemptive application by an ETF issuer seeking to tokenize shares of an exchange-traded fund, TBIL, the U.S. Treasury 3 Month Bill ETF. The proposal would record ownership on a permissioned blockchain ledger while preserving the same fund, same economics, same exchange listing and same regulatory framework. The application remains pending before the SEC, and there can be no assurance relief will be granted. That may sound like a niche legal filing. It is not. It is a test of whether capital markets modernization happens inside the regulatory perimeter or outside it.

That distinction matters to investors because the next major on-chain growth category may not be speculative tokens. It may be trusted yield, usable collateral and regulated exposure. Stablecoins already demonstrated the demand for digitally native dollars. The next logical step is digitally native instruments backed by real portfolios, real governance and real investor protections.

That is where tokenized ETFs could become powerful.

Imagine Treasury exposure that can plug into next-generation collateral networks. Imagine ETF shares that remain within familiar regulatory guardrails while operating on more modern rails. Imagine advisors and institutions accessing blockchain efficiency without having to underwrite experimental structures.

The first tokenization narrative was “replace incumbents.” The stronger narrative may be “upgrade incumbents.” That does not diminish crypto; it commercializes it.

For regulators, tokenized ETFs may offer a pragmatic path forward: enable innovation where investor protections remain intact, rather than pushing demand into parallel channels with greater uncertainty. For exchanges, custodians, brokers and market makers, it could create a new infrastructure layer around products investors already understand.

For issuers, it may become a race. The firms that combine trusted wrappers, credible assets and functional on-chain rails could capture disproportionate flows. And for allocators, the signal may be simple: blockchain technology is becoming less about novelty and more about plumbing.That is usually when real adoption begins.

The broader lesson is that distribution often beats disruption:

Who already has trusted wrappers?

Who already has liquidity?

Who already has access to advisors, retirement assets and institutions?

Who can bridge old rails and new rails fastest?

Those questions point toward ETFs.

The next trillion dollars of tokenized assets may not come from inventing something entirely new; they may come from upgrading what already works. Crypto’s first era was about building outside the system. Its next era may be about powering the system.

Headlines of the week

By Helene Braun

A few of crypto’s biggest debates converged this past week as Michael Saylor’s Strategy (MSTR) sold bitcoin to fund preferred stock dividends, JPMorgan CEO Jamie Dimon escalated his fight against yield-bearing stablecoins during the CLARITY Act debate, and Citi projected tokenized securities could grow into a $5.5 trillion market by 2030, driven by rising demand for onchain Treasuries and tokenized stocks.

Michael Saylor’s Strategy sold 32 bitcoin for $2.5 million to fund dividend payments: The 8-K filing Monday says proceeds from the May 26–31 sale, executed at an average price of $77,135 per coin, will fund distributions on Strategy’s preferred stock.

‘The banks will not accept it’: Dimon escalates battle over stablecoin rewards in CLARITY Act debate: JPMorgan CEO Jamie Dimon criticized Coinbase CEO Brian Armstrong and warned the current CLARITY Act framework could ultimately fail, as banks and crypto firms clash over whether stablecoin issuers should be allowed to offer yield-bearing rewards that resemble bank deposits.

Citi predicts the tokenized securities market will grow to $5.5 trillion by 2030: Stablecoins alone will generate a demand for up to $1 trillion worth of onchain U.S. Treasury bills and $2.6 trillion for tokenized stocks, said Citi.

Chart of the Week

RWA Perp Volume by Category: Equities Overtake Commodities (excluding oil)

RWA perps run ~$45–60 billion/week, and flow is rotating out of commodities into equities. Equities roughly tripled to ~$18 billion and just overtook the commodities (excluding oil) block, while oil faded after its April macro spike. This implies that crypto-venue derivatives are increasingly used for 24/7 equity exposure, with commodities now the episodic, event-driven slice.

Listen. Read. Watch. Engage.

Listen: Solana’s Anatoly Yakovenko Says Permissionless Systems Are Critical for Institutions.

Read: In “Crypto for Advisors”, Hassan Ahmed of Coinbase outlines the state of crypto, stablecoins and regulations in Asia, comparing growth to regions with clarity.

Watch: Bitcoin ETFs bleed $1 billion as capital rotates into HYPE, SOL, XRP.

Engage: Are you attending the ICI Conference in Nashville? Let’s connect onsite!

Looking for more? Receive the latest crypto news from coindesk.com and market updates from coindesk.com/institutions.

Note: The views expressed in this column are those of the author and do not necessarily reflect those of CoinDesk, Inc., CoinDesk Indices or its owners and affiliates.

Welcome to our institutional newsletter, Crypto Long & Short. This week:

Alex Tapscott on the stalling of the CLARITY Act and how it’s impacting the average American consumer.

Aisha Hunt writes that crypto will grow by upgrading Wall Street’s trusted products rather than replacing them.

Top headlines institutions should pay attention to by Helene Braun

“RWA Perp Volume by Category: Equities Overtake Commodities” in Chart of the Week

-Alexandra Levis

Expert Insights

What about the American consumer?

By Alex Tapscott, CEO, CMCC Global Capital Markets

The little guy is getting lost in the political horse-trading around the CLARITY Act.

The U.S. Senate Banking Committee recently advanced the Digital Asset Market CLARITY Act, legislation that, if enacted, could finally establish clear rules for digital assets in the United States. The bill has survived months of bipartisan negotiations and horse trading between banking interests and upstart fintech companies.

A bipartisan compromise brokered by Senators Thom Tillis (R-NC) and Angela Alsobrooks (D-MD) broke a log-jam that had slowed down the bill’s progress. In the end, the banks got most of what they wanted in this “deal”: the legislation explicitly prevents fintech platforms from treating stablecoins, digital assets backed by dollars, as interest bearing accounts, while still permitting them to pay rewards and bonuses, as banks and credit card issuers do.

That should have ended the debate. Yet banking lobby groups are demanding tighter restrictions to eliminate many forms of consumer rewards altogether. Clearly, they seek to squash this already compromised bill before a full Senate vote, so that it never reaches the Resolute Desk.

Lost amid the political wrangling of crypto and banking interests is the average American consumer.

According to the Consumer Financial Protection Bureau (CFPB), Americans paid roughly $5.8 billion in overdraft fees in 2023, even after years of industry efforts to reduce so-called “junk fees.” Overdraft charges disproportionately hit financially vulnerable households, with nearly 80% of fees concentrated among 9% of accounts. And then there are account minimums, wire charges and payment delays, which add friction. Meanwhile, the average savings rate is only 0.38%.

Consumers want financial services to move faster, cost less and earn them more.

Stablecoins are gaining popularity because they herald a world where digital dollars move across the internet as cheaply and seamlessly as a WhatsApp message. They can lower remittance costs, improve access to digital commerce, expedite real-time payments and create new ways for consumers to save, spend and transact online.

And Americans are asking for CLARITY because many already use these tools. According to the Crypto Council for Innovation, one in five American adults now owns cryptocurrency. That’s roughly 68.5 million people. Stablecoins are among the fastest-growing categories of digital assets, particularly among younger consumers, immigrants, freelancers and underserved communities seeking faster and cheaper financial tools. Four in five merchants believe accepting crypto could help attract new customers, while 73% of small business owners expect crypto payments to grow.

That’s what makes this debate so politically mystifying. For years, progressives argued that concentrated financial power harmed consumers and Main Street. They criticized large banks for extracting rents while lobbying against regulations that diluted bank influence. Those critiques were often correct. Today some of those progressives, like Elizabeth Warren, who championed the Consumer Financial Protection Bureau, are now defending banking profits against a technology that could inject real competition into financial services and empower consumers and small businesses.

Congress should pass CLARITY in its current form to benefit American consumers and preserve American competitiveness and leadership in the next era of financial technology. This lead is by no means assured: today, 88% of global crypto trading volume occurs on non-U.S.-based exchanges, while foreign-issued stablecoins account for 75% of stablecoin volume. Over the past decade, the U.S. share of global crypto developers has fallen from 38% to just 19%.

Do American politicians want their country to continue leading, or do they prefer watching such financial transformation from the sidelines?

In the 1990s, the Clinton administration helped usher in the commercial internet through the Telecommunications Act of 1996, a bipartisan effort expanding innovation and competition. Now, Congress has an opportunity to unleash the new internet of value by passing CLARITY.

Under GENIUS and CLARITY, stablecoin issuers must meet strong reserve requirements, transparency obligations, anti-money laundering standards, cybersecurity rules and consumer protections. Sensible public policy will unleash investment and innovation, as it did in the internet era.

This story need not end in conflict between banks and blockchains. Incumbents can just as easily embrace blockchain and its various benefits, from real-time global settlement and tokenized assets, to new forms of on-chain lending, payments, savings and commerce.

The question is whether lawmakers will vote to lead this next technological revolution and advance the interests of American consumers or cede the future to entrenched interests.

Principled Perspectives

Why Crypto May Need ETFs More Than ETFs Need Crypto

By Aisha Hunt, founder of Kelley Hunt, PLLC

Crypto spent its first decade trying to replace Wall Street. Its next trillion dollars may come from partnering with it. The first wave of tokenization focused on creating new assets, new venues and new systems outside traditional finance. Some of that innovation mattered. Much of it struggled with the same problem: markets do not scale on technology alone. They scale on trust, liquidity and distribution. That reality favors ETFs.

The ETF wrapper became one of the most successful financial products of the modern era because it solved practical investor problems at scale: low-cost access, transparency, intraday liquidity, operational simplicity and broad distribution across brokerage platforms and advisory channels.

Those advantages took decades to build. Tokenization does not erase them. In fact, it may amplify them. If blockchain rails can be integrated into ETFs, investors may not have to choose between innovation and protection. They could gain exposure to familiar products with the potential benefits of faster settlement, programmable ownership, collateral mobility and broader digital interoperability, all inside a structure already trusted by institutions, advisors and retail investors.

That is a far bigger commercial opportunity than asking trillions of dollars to migrate into unfamiliar vehicles. This is why one underappreciated development matters. On January 21, 2026, F/m Investments LLC and The RBB Fund, Inc. filed what is believed to be the first exemptive application by an ETF issuer seeking to tokenize shares of an exchange-traded fund, TBIL, the U.S. Treasury 3 Month Bill ETF. The proposal would record ownership on a permissioned blockchain ledger while preserving the same fund, same economics, same exchange listing and same regulatory framework. The application remains pending before the SEC, and there can be no assurance relief will be granted. That may sound like a niche legal filing. It is not. It is a test of whether capital markets modernization happens inside the regulatory perimeter or outside it.

That distinction matters to investors because the next major on-chain growth category may not be speculative tokens. It may be trusted yield, usable collateral and regulated exposure. Stablecoins already demonstrated the demand for digitally native dollars. The next logical step is digitally native instruments backed by real portfolios, real governance and real investor protections.

That is where tokenized ETFs could become powerful.

Imagine Treasury exposure that can plug into next-generation collateral networks. Imagine ETF shares that remain within familiar regulatory guardrails while operating on more modern rails. Imagine advisors and institutions accessing blockchain efficiency without having to underwrite experimental structures.

The first tokenization narrative was “replace incumbents.” The stronger narrative may be “upgrade incumbents.” That does not diminish crypto; it commercializes it.

For regulators, tokenized ETFs may offer a pragmatic path forward: enable innovation where investor protections remain intact, rather than pushing demand into parallel channels with greater uncertainty. For exchanges, custodians, brokers and market makers, it could create a new infrastructure layer around products investors already understand.

For issuers, it may become a race. The firms that combine trusted wrappers, credible assets and functional on-chain rails could capture disproportionate flows. And for allocators, the signal may be simple: blockchain technology is becoming less about novelty and more about plumbing.That is usually when real adoption begins.

The broader lesson is that distribution often beats disruption:

Who already has trusted wrappers?

Who already has liquidity?

Who already has access to advisors, retirement assets and institutions?

Who can bridge old rails and new rails fastest?

Those questions point toward ETFs.

The next trillion dollars of tokenized assets may not come from inventing something entirely new; they may come from upgrading what already works. Crypto’s first era was about building outside the system. Its next era may be about powering the system.

Headlines of the week

By Helene Braun

A few of crypto’s biggest debates converged this past week as Michael Saylor’s Strategy (MSTR) sold bitcoin to fund preferred stock dividends, JPMorgan CEO Jamie Dimon escalated his fight against yield-bearing stablecoins during the CLARITY Act debate, and Citi projected tokenized securities could grow into a $5.5 trillion market by 2030, driven by rising demand for onchain Treasuries and tokenized stocks.

Michael Saylor’s Strategy sold 32 bitcoin for $2.5 million to fund dividend payments: The 8-K filing Monday says proceeds from the May 26–31 sale, executed at an average price of $77,135 per coin, will fund distributions on Strategy’s preferred stock.

‘The banks will not accept it’: Dimon escalates battle over stablecoin rewards in CLARITY Act debate: JPMorgan CEO Jamie Dimon criticized Coinbase CEO Brian Armstrong and warned the current CLARITY Act framework could ultimately fail, as banks and crypto firms clash over whether stablecoin issuers should be allowed to offer yield-bearing rewards that resemble bank deposits.

Citi predicts the tokenized securities market will grow to $5.5 trillion by 2030: Stablecoins alone will generate a demand for up to $1 trillion worth of onchain U.S. Treasury bills and $2.6 trillion for tokenized stocks, said Citi.

Chart of the Week

RWA Perp Volume by Category: Equities Overtake Commodities (excluding oil)

RWA perps run ~$45–60 billion/week, and flow is rotating out of commodities into equities. Equities roughly tripled to ~$18 billion and just overtook the commodities (excluding oil) block, while oil faded after its April macro spike. This implies that crypto-venue derivatives are increasingly used for 24/7 equity exposure, with commodities now the episodic, event-driven slice.

Listen. Read. Watch. Engage.

Listen: Solana’s Anatoly Yakovenko Says Permissionless Systems Are Critical for Institutions.

Read: In “Crypto for Advisors”, Hassan Ahmed of Coinbase outlines the state of crypto, stablecoins and regulations in Asia, comparing growth to regions with clarity.

Watch: Bitcoin ETFs bleed $1 billion as capital rotates into HYPE, SOL, XRP.

Engage: Are you attending the ICI Conference in Nashville? Let’s connect onsite!

Looking for more? Receive the latest crypto news from coindesk.com and market updates from coindesk.com/institutions.

Note: The views expressed in this column are those of the author and do not necessarily reflect those of CoinDesk, Inc., CoinDesk Indices or its owners and affiliates.

Revolut has announced plans to launch a U.S. bank next year, offering FDIC-insured accounts and stablecoin services as it deepens its push into American financial services.

Reuters reported, citing newly appointed Revolut U.S. CEO Cetin Duransoy, that the British fintech plans to offer high-yield investment accounts, checking accounts, stablecoins, multi-currency deposits, stock trading, and crypto trading through its U.S. platform.

The company does not plan to open physical branches in the United States, Reuters reported. Duransoy told the news agency that customers will instead get access to ATM networks.

Revolut targets U.S. banking charter

Revolut filed an application for a U.S. national bank charter with the Office of the Comptroller of the Currency in early March, according to Reuters. The filing came after the company dropped an earlier plan to buy a U.S. lender. According to the report, the proposed bank will be based in Stamford, Connecticut, with another office in New York.

Duransoy told Reuters that Revolut will first focus on business and retail customers who need access to several currencies. He said those customers may need dollars, rupees, or Latin American currencies. The company’s app already supports services in more than 30 currencies, according to the report.

Stablecoins sit beside traditional accounts

In the U.S., Revolut plans to combine insured banking products with crypto-linked services, according to Reuters. The planned product list includes FDIC-insured checking accounts and high-yield investment accounts, while the same platform will also offer stablecoins and digital asset trading.

The report places Revolut’s application within a new round of bank charter filings from firms tied to crypto and fintech. Reuters said U.S. regulators, including the OCC, have taken a more open approach toward such applications.

Kraken became the first crypto-native company to receive a “skinny” master account with the Federal Reserve in March, according to the report. Reuters said the account gives Kraken direct access to core U.S. payment systems.

U.S. expansion remains a key goal

Revolut serves 75 million customers globally, Reuters reported. The company has about 1 million U.S. customers, many of whom first used the app while traveling or living in Europe, Latin America, or Asia, according to Duransoy.

The U.S. plan follows Revolut’s long-running effort to build what it has called “the world’s first truly global bank.” Earlier this year, the company received approval to launch a fully licensed bank in the United Kingdom, according to the report.

Revolut reported revenue of 4.5 billion pounds, or about $6 billion, last year, according to Reuters. The company also posted a net profit of 1.3 billion pounds, or about $1.75 billion.

The privately held fintech was valued at $75 billion in its latest funding round, Reuters reported. CEO Nik Storonsky has said publicly that the company does not plan to list shares before 2028.

At the same time, Revolut has expanded its crypto work. Last year, the firm tapped Polygon to support remittances, POL staking, and crypto card payments in its main app. The company was also selected by the Financial Conduct Authority to join a fiat-pegged stablecoin sandbox payments trial, according to the report.

3June2026 – Tether, the largest company in the digital asset industry, today announced the launch of the world’s first gold-backed neobanking Visa card in collaboration with Fasset, a digital banking and investment platform that allows users to receive money, invest, earn, and make payments from anywhere in the world. This marks a strategic step toward mainstream use cases for tokenized gold on a global and relatable scale.

The card will operate on the Visa network, enabling users to spend fiat at merchant stores worldwide where Visa cards are accepted while earning up to 6% cashback in XAU₮ on eligible transactions, creating a reward layer tied to Tether’s gold-backed assets. Users can seamlessly spend their assets in seconds by converting XAU₮ to USD₮ and then to fiat at the point of transaction. Additionally, the card will feature an automatic round-up function that auto-invests the spare change from every transaction in XAU₮, enabling continuous, passive gold accumulation through everyday spending.

Fasset brings together multi-currency accounts, fast transfers, instant settlements, a global debit card, and access to interest-free investments across crypto, stocks, funds, and commodities on its platform. With a presence across Asia and Africa, it also operates as one of the largest digital asset off-ramp providers in its region, ensuring the USD₮-to-fiat conversion layer is optimized for speed and reliability.

This initiative introduces a new global payment model that combines the accessibility of digital assets with the long-standing stability of gold. It reflects the next phase of gold-backed asset usage by embedding these assets into familiar financial experiences. The card will be integrated directly with Fasset’s wallet infrastructure, with XAU₮ cashback flowing into users’ wallets in real time.

The market cap of tokenized digital gold is over $5.3 billion, with XAU₮ accounting for over $2.6 billion. Demand is growing for digital assets that offer Investment opportunities, high liquidity, accessibility, and usability, especially in emerging markets where currency volatility is a challenge. Tether continues to expand its reach by collaborating with platforms to meet these needs. As part of the launch, Tether is committing up to $1 million in XAU₮ to power the card’s rewards ecosystem and accelerate the real-world use of tokenized gold.

“Historically, gold has been a store of value, not a medium of exchange. This initiative changes that narrative,” said PaoloArdoino,CEOofTether. “By collaborating with systems that make digital assets practical and accessible globally, we are extending the utility of our ecosystem. Through this initiative, we are connecting stablecoins and tokenized gold to real-world payment systems, making them usable, accessible, and seamlessly integrated into global transactions, giving users the option to hold gold and invest it however they choose, without friction or borders.”

MohammadRaafiHossain,CEOandCo-FounderofFasset, said: “For over a thousand years, gold has been the most trusted store of wealth across our markets. We’re bringing it into the digital age. With $32 billion in annualized volume (95% in real-world assets) and the world’s first gold-backed neobanking card, Fasset is building the infrastructure to make Tether Gold the most widely held digital gold token in emerging markets. This isn’t just a card – it enables the adoption of digital gold at scale through Fasset’s extensive distribution network.”

Fasset’s infrastructure and distribution in high-growth markets, combined with Tether’s global liquidity and asset issuance capabilities, enable this collaboration to scale rapidly across regions where demand for stable, asset-backed financial tools is rising. Together, the companies are creating a global infrastructure for the future of asset-backed banking, connecting thousands of years of gold heritage with modern blockchain technology.

About Tether Gold (XAU₮)

Tether Gold (XAU₮) is a digital asset offered by TG Commodities Limited. One full XAU₮ token represents one troy fine ounce of gold on a London Good Delivery bar. The token can be traded or moved easily at any time, anywhere in the world, and can be transferred to any on-chain address from the purchaser’s Tether wallet, where it is issued after purchase. The allocated gold is identifiable with a unique serial number, purity, and weight, and is redeemable in the form of physical gold.

Important Note:

This press announcement is not an offer to sell or the solicitation of an offer to buy Tether Gold (XAU₮). TG Commodities S.A de C.V. will only sell or redeem XAU₮ pursuant to its gold token terms of sale and service available (as of the date of this press release) at https://gold.tether.to/legal

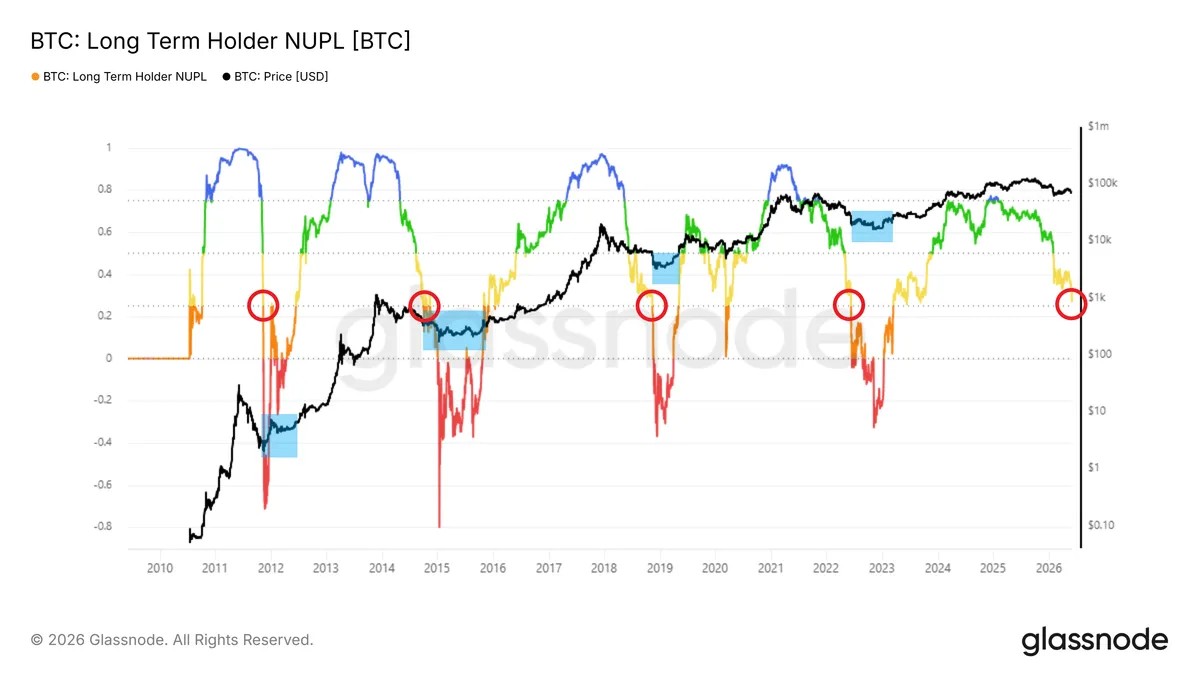

Bitcoin ($BTC) trades near $67,002, and on-chain data from Glassnode shows the long-term holder cohort is signaling more downside before this bear market prints a cycle low.

Three Glassnode charts point in the same direction. Holders carrying coins for over 155 days appear stressed. Yet they have not reached the pain levels that historically marked the floor of past Bitcoin cycles.

Long-Term Holder NUPL Slides Into the Historical Bottom Zone

Bitcoin Long-Term Holder Net Unrealized Profit and Loss (LTH NUPL) sits near 0.25 (red circle). That reading marks the upper edge of the orange band that has framed every prior cycle floor.

Historically, every prior touch of this zone aligned with the lowest $BTC prices of the cycle (blue zones). The 2012, 2015, 2019, and 2022 bottoms all formed inside the orange band.

Long term holder NUPL / Source: Glassnode

Meanwhile, the signal has not flipped to accumulation yet. NUPL must push deeper into the orange or red band, similar to past cycle bottoms.

Long-Term Holder Supply Just Hit a New All-Time High

While NUPL signals near-term pain, the supply held by long-term holders has quietly printed a fresh all-time high. The cohort now controls roughly 15 million $BTC, the highest figure on record.

This pattern repeats in every cycle. During the mid-phase of a Bitcoin bear market, long-term holders absorb coins from short-term sellers.

They then distribute that supply into the next uptrend, often months or years later. The current rhythm of accumulation suggests the cohort sees value here, even as price corrects further.

Total supply held by long-term holders / Source: Glassnode

However, this same setup confirms the broader market is still in the bearish leg. Long-term holders rarely sell into weakness. The current selling pressure is coming from a younger, less conviction-driven cohort.

$BTC Price Could Test $56,000 Before True Capitulation

The third Glassnode chart frames the magnitude question. Bitcoin LTH Relative Unrealized Loss sits at 15.5%. Roughly 15 cents of every dollar in long-term holder portfolios is underwater.

Cycle bottoms in 2019 and 2022 pushed this metric above 50%. Therefore, the distance between today’s reading and that historical floor signals the bear has further to run. Glassnode wrote on X:

“At $69.5k, LTH Relative Unrealized Loss sits at 15.5%. For every dollar long-term holders’ bags are worth today, they are carrying roughly 15 cents in unrealized loss. At cyclical extremes, that number has exceeded 50 cents on the dollar. Stress is present, but the long-term holder base remains far from the levels of pain that have historically marked cycle lows.”

Long term holder relative unrealized loss / Source: X

A drawdown into the $56,000 zone would lift relative unrealized loss toward 30 to 40%. That area marks a critical long-term support cluster and would put on-chain stress in line with early phases of past capitulations.

A deeper flush to the $44,000 area cannot be ruled out if NUPL slides into the red zone. Reclaiming $105,000 would invalidate this bearish thesis by pushing long-term holders back into broad profit. Such a move would echo the rare signal seen at past cycle reversals.

$BTC trades down 11.6% over the past week and 36.3% over the past year. Based on long-term holder data, the path of least resistance points lower before higher.